If you’re an ambitious Mortgage Loan Officer looking for a way to build a high-income career with work-from-home freedom, the answer often boils down to one word: specialization. While many MLOs try to be everything to everyone, the most successful ones carve out a specific niche and absolutely own it.

One of the most profitable and personally rewarding niches you can dive into right now is serving first-time homebuyers.

Your Next Big Opportunity: First-Time Homebuyers

This isn’t just a small market segment; it’s a massive, continuous wave of potential clients who are more in need of expert guidance than anyone else. They’re actively looking for a trusted professional to help them navigate everything from FHA loans to local down payment assistance programs.

When you become that expert, you’re not just closing a single loan. You’re building a foundation of trust that can lead to a lifetime of referrals.

Why This Market Is a Goldmine for MLOs

The reality is, the demand for loan officers who genuinely understand first time home buyer programs is skyrocketing. Younger generations are hitting their prime home-buying years, and they’re eager to own a piece of the American dream.

But they’re also facing real-world challenges, like student loan debt and the struggle to save for a down payment. This is precisely why specialized assistance programs are so crucial for them—and why they need an MLO who knows these programs inside and out.

Becoming the go-to MLO for first-time buyers means you stop chasing leads and start attracting clients. Your expertise becomes a magnet for those who need you most, creating a reliable and ever-growing business pipeline.

To really connect with and support this key demographic, providing resources like a comprehensive first time homebuyer guide can empower them to make confident choices. When you can clearly explain the ins and outs of various programs, you stop being just a loan originator and become an indispensable advisor. That shift is what builds incredible client loyalty and drives your high-commission income.

Positioning Yourself for Success

Tapping into this lucrative market starts with a solid foundation of knowledge. Our fully online education, fully approved by the NMLS Nationwide Multi State Licensing System and Registry, makes it easy to get your Mortgage Loan Originator license and gain the specific expertise needed to serve these buyers effectively.

Our curriculum, which includes our exam prep package for free, digs into the essential programs and regulations that are vital for succeeding in this niche.

Once you master this material, you’ll be able to:

- Confidently explain complex loan options in simple, easy-to-understand terms.

- Pinpoint the best assistance programs for a client’s unique financial situation.

- Build a powerful reputation as the local expert for first-time buyers.

This career isn’t just about high earning potential. It’s about the flexibility to set your own hours and build a business that truly fits your life. It all starts with getting the right education and the right tools to step into this rewarding specialty with confidence.

Getting Inside the Head of Today’s First-Time Home Buyer

If you want to truly connect with first-time homebuyers, you have to get to know them. We’re not talking about a single, uniform group; they’re a diverse generation wrestling with a very specific set of financial and social realities that completely shape their journey to owning a home.

Many of today’s aspiring homeowners are staring down a mountain of student loan debt while juggling the high cost of just about everything else. It’s no wonder the traditional 20% down payment feels less like a goal and more like a fantasy. This constant financial squeeze has totally rewired how they think about big purchases, especially real estate.

Bridging the Trust Gap

One of the biggest things to understand about this demographic is their deep-seated skepticism. Many feel like the traditional financial system is rigged against them, and that’s created a massive gap in trust. This is where you have a golden opportunity to be different.

The data backs this up. The NextGen Homebuyer Report found that while a staggering 95% of buyers between 18 and 44 want to own a home, their confidence is shaky. It’s pushed them to look for answers everywhere but the traditional places—turning to AI tools and TikTok for advice instead of professionals. You can read the full report on NextGen Homebuyers to see just how much the game has changed.

You bridge that gap by becoming an educator first and a loan officer second. Your job isn’t just about pushing paper; it’s about making the mortgage process clear, patiently answering every question, and pulling back the curtain on what can be an intimidating industry. When you do that, you stop being a salesperson and become a trusted guide—which is exactly what they’re looking for.

The Financial Hurdles and How You Can Help

Let’s be honest: for most first-timers, the biggest roadblock is money. They’re trying to make sense of a tangled mess of income, debt, and savings, and it’s easy to feel completely lost.

Here are the main challenges you’ll see again and again:

- Saving for a Down Payment: When rent and everyday costs keep climbing, trying to stash away a huge pile of cash feels next to impossible.

- Managing Student Debt: Hefty student loan payments can seriously cramp their borrowing power.

- Understanding Credit Scores: Many don’t have a solid grasp on how their credit history impacts their chances of getting a loan or the interest rate they’ll pay.

- Calculating Debt-to-Income Ratio: This is a make-or-break number that a lot of people find confusing, even though it’s central to getting approved.

As a sharp MLO, your value skyrockets when you can break these things down into simple, manageable pieces. For example, you can help them get a crystal-clear picture of their financial standing. Our guide is a great resource when you need to explain how to calculate debt-to-income ratio to your clients. This educational approach doesn’t just inform them; it empowers them to take the next step.

When you can show a client a clear, actionable path to homeownership—perhaps by connecting them with a down payment assistance program or an FHA loan with a low down payment—you become an indispensable asset.

Ultimately, your success comes down to empathy and education. When you understand the unique pressures and preferences of modern first-time buyers, you can tailor your entire approach to what they actually need. That client-first focus is the secret to building a thriving, commission-based career with the freedom you want, powered by a pipeline of grateful, loyal clients. The future looks bright—almost #FACC00 bright.

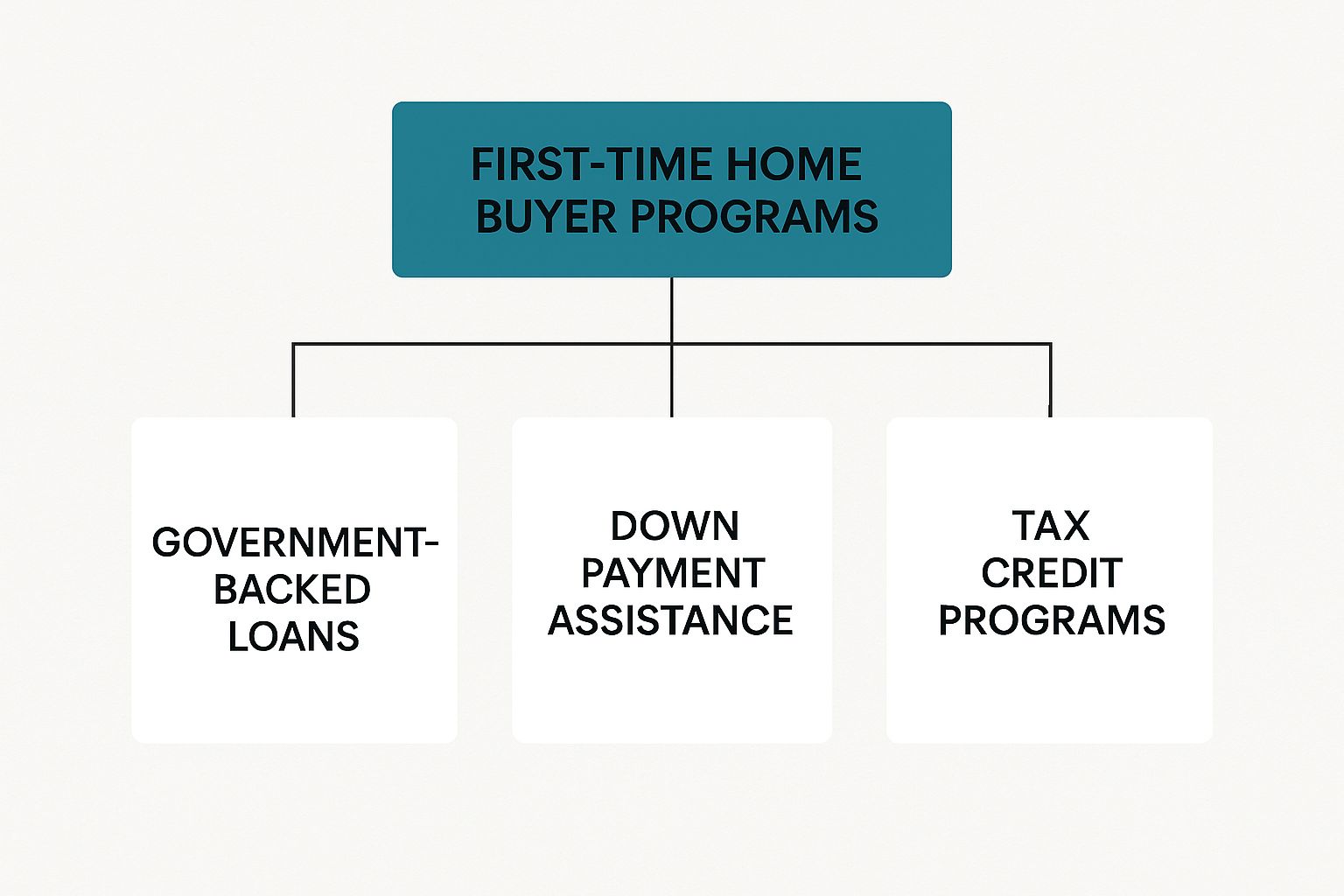

A Loan Officer’s Guide to Key First-Time Home Buyer Programs

As a Mortgage Loan Officer, your knowledge of first-time home buyer programs is more than just a tool—it’s your superpower. These aren’t just obscure loan products; they’re the keys that unlock the door to homeownership for people who thought it was impossible. When you master these programs, you stop being just another MLO and become a genuine problem-solver, an essential guide your clients will rely on.

Think about the biggest hurdles your clients face: scraping together a down payment and meeting tough credit standards. Your expertise directly tackles these fears. When you can confidently lay out clear, simple solutions, you pave a direct path to the closing table. This is exactly the kind of practical knowledge our online education, fully approved by the NMLS, is built to provide, setting you up to be the go-to expert in your market.

This visual breakdown shows the main types of assistance out there, helping you see the different paths to homeownership you can offer your clients.

As you can see, a successful deal often isn’t about finding one perfect program. It’s about creatively combining a government-backed loan with a down payment assistance program, giving you multiple ways to structure an approval.

Decoding Federal Government-Backed Loans

Federal programs are the foundation of first-time homebuyer financing. They’re designed to make mortgages more accessible by having the government insure the loan. This safety net reduces the risk for lenders, which in turn allows them to offer much more favorable terms to borrowers.

For MLOs, there are three main workhorses you’ll use day in and day out:

- FHA Loans: Insured by the Federal Housing Administration, these are a perennial favorite for first-timers. Why? Because they come with a low 3.5% down payment requirement and have forgiving credit score guidelines. They’re the perfect fit for clients who have a steady income but just haven’t had the time to save up a massive down payment.

- VA Loans: These are an incredible benefit for eligible veterans, active-duty service members, and their surviving spouses. The star of the show here is the 0% down payment option. On top of that, VA loans don’t require private mortgage insurance (PMI), which can save your clients hundreds of dollars every single month.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are aimed at helping people buy in rural and suburban communities. Just like VA loans, they offer the chance for a 0% down payment. They are a fantastic option for clients wanting to move a little further out from the major city centers—a trend that’s becoming more and more popular.

Understanding the fine print of each program lets you instantly match a client’s situation to the right loan, building immediate trust and showing them you’re on their side.

The Power of Down Payment Assistance Programs

Let’s be honest: for most first-time buyers, the down payment is the single biggest mountain to climb. This is where Down Payment Assistance (DPA) programs become your secret weapon. These are typically run by state or local agencies and provide cash to cover some or all of the down payment and closing costs.

DPA isn’t a one-size-fits-all solution. The help comes in a few different flavors:

- Grants: This is the best-case scenario—free money that never has to be paid back.

- Forgivable Loans: These are 0% interest loans that are forgiven over time, usually after the buyer lives in the home for a certain number of years.

- Low-Interest Loans: These are essentially small second mortgages with very low or deferred payments, designed to get the buyer over the initial financial hump.

By taking the time to research and master the DPA programs in your specific state, you immediately stand out from the crowd. You become the MLO who can find a way to make it happen when others say it’s impossible.

A Closer Look at State and Local Programs

While federal loans are the same everywhere, many of the most powerful programs are run at the state and local levels. Every state has a Housing Finance Agency (HFA) that offers its own unique menu of options for residents.

These agencies might offer special bond programs with below-market interest rates or even tax credits for first-time buyers. As an MLO who wants to specialize in this market, your first job is to become an expert on what your local HFA offers. Knowing these details can be the one thing that gets a tricky deal across the finish line, making you a hero to your clients and a top partner for real estate agents.

Top Ten Cities for First Time Home Buyers

Specializing in this niche is especially lucrative in cities with a high concentration of younger buyers. Recent statistics highlight the top ten U.S. cities where first-time buyers are making the biggest impact. Focusing your marketing efforts in these areas can yield incredible results.

| City, State | First-Time Buyer Market Share |

|---|---|

| Minneapolis, MN | 55% |

| Buffalo, NY | 54% |

| St. Louis, MO | 53% |

| Louisville, KY | 52% |

| Hartford, CT | 52% |

| Birmingham, AL | 51% |

| Pittsburgh, PA | 51% |

| Virginia Beach, VA | 50% |

| Detroit, MI | 50% |

| Richmond, VA | 50% |

As you can see, in cities like Minneapolis, first-time buyers make up over half the market. This represents a massive opportunity for MLOs who know how to connect with and serve this demographic. This kind of specialized knowledge, combined with our online courses and free exam prep, is your roadmap to a high-commission career that also gives you the work-life balance you’re looking for. To round out your professional toolkit, take a look at these expert mortgage broker tips to gain an edge in this competitive market.

Marketing Your Expertise to Attract First-Time Buyers

You can know every first time home buyer program inside and out, but that knowledge only turns into a paycheck when potential clients know you’re the one holding the keys. This is where smart marketing comes into play. The goal isn’t just to get your name out there; it’s to become the go-to expert—that trusted, approachable pro who can make their homeownership dream a reality.

Forget about flashy, expensive ad campaigns. Real, effective marketing is all about consistently showing people your value. When you create genuinely helpful and educational content, you build trust. Before you know it, you’ll start attracting clients who are already searching for the exact solutions you offer. This is how you build a thriving business with serious commission potential, all while enjoying the freedom of working from home and naming your own hours.

Building Your Digital Presence

In this day and age, your online presence is your storefront. It’s the first place first-time buyers will go to check you out and decide if you’re the right person to guide them through this huge life step. The secret is to be a teacher, not a salesperson.

First things first, get your professional website or landing page in order. It should scream, “I help first-time buyers!” Make sure you’re using keywords that people are actually typing into Google, like “first time home buyer programs in [Your City]” or “down payment assistance help.” This is how they find you.

Once your home base is set, it’s time to cast a wider net with content that actually helps people:

- Social Media Videos: Think short, simple, and to the point. Hop on Instagram or TikTok and create a 60-second video explaining a DPA program. Break down the basics of an FHA loan. Share a quick success story from a client who just got their keys (with their permission, of course!).

- Educational Blog Posts: Write articles that answer the questions you get asked over and over. Think about topics like “5 Ways to Qualify for Down Payment Help in Texas” or “What Credit Score Do I Really Need for My First Home?” This kind of content brings in organic traffic and instantly positions you as an authority.

- Free Informational Webinars: Host a free online session once a month to walk people through the home-buying basics. It’s a fantastic way to connect with dozens of potential clients at once and show off what you know in a completely no-pressure setting. A touch of the color #29abe3 in your slides can give your presentation a modern and trustworthy vibe.

Your digital marketing shouldn’t feel like a sales pitch. It should feel like you’re giving away your best advice for free. When you generously share valuable information, you build a loyal audience that will come straight to you when they’re ready to buy.

Forging Powerful Offline Connections

While a solid digital footprint is a must-have, don’t ever underestimate the power of old-fashioned, real-world networking. The most successful MLOs I know have built a rock-solid referral network that keeps their pipeline full of qualified clients.

Real estate agents are your most important allies here. They’re on the front lines, meeting hopeful first-time buyers every single day. When an agent knows you’re the one who can get their clients approved using these specialized programs, you become an indispensable part of their team. This relationship is so critical; you can learn more about the top ways mortgage brokers can network with real estate agents to really supercharge your business.

But don’t stop with agents. Think about connecting with:

- Managers of local apartment complexes who know exactly which tenants are itching to buy.

- Financial planners whose clients are in the process of saving up for their first home.

- HR managers at big local companies who often work with employees relocating to your area.

When you blend a savvy digital strategy with strong local networking, you create a powerful, self-sustaining marketing machine that consistently brings your ideal clients right to your door. This is the foundation of a successful, high-income career as an MLO who specializes in the incredibly rewarding first-time home buyer market.

Mortgage Brokers Get Newbies the Best Rates through Wholesale Mortgage Promotional Programs for 1st Time Home Buyers

As a Mortgage Loan Officer, your edge often comes from knowing where to look beyond the obvious. While big retail banks offer a standard, fixed menu of loan products, independent mortgage brokers have a secret weapon: the wholesale mortgage channel. Think of it as your backstage pass to a much bigger world of loan options and better interest rates for your clients.

For a first-time homebuyer, this access can be a complete game-changer. Suddenly, they aren’t stuck with one bank’s strict rules or take-it-or-leave-it rates. You become their personal shopper, taking their loan application to dozens of wholesale lenders to hunt down the absolute best deal. This is how you turn the dream of owning a home into a tangible, affordable reality for more people.

The Wholesale Advantage for First-Time Buyers

Wholesale lenders operate behind the scenes; they don’t have public-facing branches or work directly with borrowers. Their entire business model is built around partnering with independent mortgage brokers like you. Because they are constantly competing for your business, they get creative, rolling out special programs and niche loan products to attract certain types of buyers—especially first-timers.

This competition creates a perfect win-win. Lenders get a steady flow of high-quality loan applications from you, and in return, you get exclusive deals to pass on to your clients. These benefits often include:

- Lower Interest Rates: With less overhead than massive retail banks, wholesale lenders can often afford to offer more aggressive rates.

- Reduced Fees: Many wholesale programs feature lower origination fees or offer lender credits to help your clients reduce their closing costs.

- Flexible Underwriting: Some wholesale lenders are specialists. They might have more forgiving guidelines for credit scores or debt-to-income ratios, opening doors for buyers who don’t fit the perfect mold.

Working the wholesale channel means you can often find a home for a loan that a traditional bank would have rejected. This problem-solving ability is what builds a rock-solid reputation and a thriving, commission-based business. You can get a deeper look at how these two worlds differ in our guide on mortgage brokers vs. bank lenders.

Positioning Yourself as a Powerful Advocate

Your real job as a broker isn’t just processing paperwork. You’re a market expert and a fierce negotiator fighting for your client. You take their one application and make lenders compete for it, forcing them to bring their best offer to the table. That’s a level of service and value a loan officer at a single bank simply can’t match.

This advocacy is more critical than ever. The latest data highlights the ongoing affordability crunch for new buyers. Many are trying to balance student debt, car payments, and other obligations, making it tough to stay under the preferred debt-to-income (DTI) ratio, which often sits around 45%. Because of this, buyers are desperately seeking creative solutions like down payment assistance. Staying on top of the latest first-time home buyer trends will keep you one step ahead.

When you can confidently tell a first-time buyer, “I’m going to shop your loan with a dozen different lenders to find you the absolute best rate and program,” you’ve just provided immense value and peace of mind.

This is the approach that closes more loans and builds a business that gives you the freedom you want, whether that means working from home or naming your own hours. Our online education, fully approved by the NMLS and including a free exam prep package, provides the foundation you need to step into this powerful role. We make getting licensed easy, so you can start helping first-time buyers and unlock the massive potential of the wholesale mortgage market.

Common Questions About Serving First-Time Buyers

Diving into a new specialty always brings up a few questions. Focusing on first-time homebuyer programs can be an amazing move for your career, but it’s totally normal to wonder about the details before you jump in. Let’s tackle some of the most common questions Mortgage Loan Officers have when they’re thinking about this high-income, commission-based niche.

My goal here is to give you clear, straight-up answers that show you just how doable and profitable this path really is. Once you see the value in becoming the go-to expert for new buyers in your area, you’ll understand how it builds a business that lasts—one that gives you the freedom to work from home and name your own hours.

How Long Does It Take to Master These Programs?

Honestly, you can get up to speed much faster than you think. While our NMLS-approved online education (which includes our exam prep package for free) gives you the foundation right away, the real key is a sharp focus.

You don’t need to know every single program out there. Start by mastering the top 3-4 programs that are most popular in your state. By zeroing in like this, you can build true expertise in a matter of weeks. Given the high-commission potential here, that focused effort pays off almost immediately.

Are First-Time Home Buyers Harder to Work With?

It’s true they need more hand-holding, but that’s exactly where your value shines. They’re navigating a complex process for the first time, and by breaking it down and patiently educating them, you become more than just their MLO—you become their trusted guide for life. Using a stable, trustworthy color like #023374 in your branding can even help reinforce that feeling of security.

Think of the extra time you spend upfront as a long-term investment. A happy first-time buyer doesn’t just come back for their next home; they become a walking, talking referral machine for you. This is the bedrock of a sustainable business that lets you work from anywhere.

How Do I Find Local and State-Specific Programs?

Knowing how to dig up local programs is a crucial skill, but it’s simpler than it sounds. Your first stop should always be your state’s Housing Finance Agency (HFA) website. They’re the ones who manage the bulk of the Down Payment Assistance (DPA) programs and other local aid.

Beyond that, your network is your best friend. Build solid relationships with experienced real estate agents—they’re often the first to know about new or updated programs. Our training actually walks you through exactly how to find and use these resources, so you can confidently find the best fit for your clients, no matter where they live.

How Do Wholesale Lenders Help Me Compete for These Buyers?

Think of wholesale lenders as your secret weapon. They are constantly competing for your business, which means you get to pass on better rates and more flexible loan options to your clients. This gives you a massive leg up on retail banks that are stuck with a single, limited menu of products.

What’s more, many wholesale lenders design loan products and run special promotions specifically for first-time buyers—deals you just can’t get anywhere else. Having this kind of exclusive access lets you offer superior solutions, making you the obvious choice for any new buyer looking for the best deal possible.

Are you ready to build a high-income career with the freedom to work from home? 24hourEDU makes getting your Mortgage Loan Originator license straightforward and easy. Our fully online education, fully approved by the NMLS Nationwide Multi State Licensing System and Registry, includes our exam prep package for free, giving you everything you need to confidently step into the rewarding world of helping first-time homebuyers. Get started today at 24hourEDU.