So, you’ve got your MLO license. That’s the first big step. Now comes the part that keeps you in the game: your annual continuing education, or CE.

Think of it as a mandatory professional tune-up. It’s the required training that keeps your license active and ensures you’re up-to-date on all the industry laws, ethics, and best practices needed to legally originate loans.

Understanding Your Annual CE Requirements

For every single Mortgage Loan Originator, completing your annual continuing education is completely non-negotiable. It’s the bedrock of your license renewal, mandated by the Nationwide Multi State Licensing System and Registry (NMLS). This isn’t just about ticking a box on a form; it’s a critical process designed to protect consumers and uphold high standards across the mortgage world.

The mortgage industry is anything but static. Regulations shift, consumer protection laws get updated, and new ethical challenges pop up all the time. Just look at the Consumer Financial Protection Bureau (CFPB)—they frequently issue new guidance on everything from junk fees to appraisal oversight. Your annual CE makes sure you’re always working with the latest information, which is absolutely essential for compliance.

Why CE Is More Than Just a Requirement

Fulfilling your yearly educational duties is a direct investment in your career. It sharpens your professional edge and reinforces your expertise. Think of it this way: a surgeon is always learning new procedures, and a mechanic has to know the ins and outs of new engine models. In that same spirit, MLOs have to stay informed to give the best—and most compliant—service to their clients.

This yearly update helps you navigate complex situations with total confidence. It dives into the key areas that directly impact your day-to-day work, including:

- Federal Law Updates: Keeping you in the loop on changes to critical regulations.

- Ethics and Fraud Prevention: Giving you real-world scenarios to strengthen your decision-making.

- Non-Traditional Mortgage Products: Broadening your knowledge of the diverse lending options out there.

This commitment to learning doesn’t just protect your license—it builds trust with your clients. When you can speak with authority about the latest industry standards, you establish yourself as a reliable and expert advisor. In a competitive market, that’s a huge differentiator. The good news is, finding and finishing your coursework can be a simple and straightforward experience.

The core purpose of mortgage continuing education is to ensure that MLOs maintain the high level of knowledge and ethical standards required to originate loans responsibly, protecting both the consumer and the integrity of the financial system.

Making the Process Easy

Navigating your CE requirements doesn’t have to be a headache. With online education, you can knock out your required hours from literally anywhere. Plus online MLO education programs like ours include a toll free line up front, offering an extra layer of support to help you succeed. It’s an effective approach that makes it easy to get the education you need to stay licensed and thrive. So many other companies try to hide their phone line from customers, but 24hourEDU does not do this. Support is one of our strengths, as well as a benefit to our students.

When you start seeing your annual CE as an opportunity for growth instead of just an obligation, you turn a mandatory task into a powerful tool for your career. You can explore a variety of flexible mortgage continuing education courses designed to fit your schedule and help you hit your renewal goals without the stress. At the end of the day, staying compliant is the key to a long and successful career as an MLO.

Breaking Down the NMLS 8-Hour CE Course

The cornerstone of your annual license renewal is the standard 8-hour mortgage continuing education course. Don’t think of it as one long, monotonous class. Instead, it’s a structured curriculum broken into specific, practical modules, each designed to keep you sharp in the areas that matter most in today’s lending world.

Once you understand the structure, the whole process feels less like a chore and more like a targeted tune-up for your career. This isn’t about memorizing obscure regulations; it’s about staying current on the practical application of the laws and ethics that guide your work every single day.

Let’s unpack what those eight hours actually cover. The NMLS has a clear breakdown to ensure every MLO is on the same page, focusing on the most critical aspects of the job.

| Topic Area | Required Hours | Key Focus Points |

|---|---|---|

| Federal Law | 3 Hours | Updates on key legislation like TILA, RESPA, and TRID. Focuses on consumer protection and disclosure requirements. |

| Ethics | 2 Hours | Real-world scenarios involving fraud prevention, fair lending, and professional conduct. |

| Non-Traditional Mortgage Products | 2 Hours | Training on loan types beyond conventional mortgages, such as adjustable-rate, interest-only, and other unique products. |

As you can see, the requirements are designed to be a practical, well-rounded refresher that directly impacts your day-to-day responsibilities. It’s all about maintaining a high standard of professionalism and compliance.

The Federal Law Component: 3 Hours

The biggest chunk of your CE—a full 3 hours—is dedicated to Federal Law. This is the backbone of your compliance knowledge, making sure you’re up to speed on the regulations that shape our industry. It’s where you’ll get a refresher on major legislation and, more importantly, any recent changes or amendments.

You can expect to cover key topics like:

- The Truth in Lending Act (TILA)

- The Real Estate Settlement Procedures Act (RESPA)

- The TILA-RESPA Integrated Disclosure (TRID) rule

Staying current here is non-negotiable. It’s what keeps you from making costly compliance mistakes and helps you serve your clients with accuracy and confidence.

Upholding Professional Ethics: 2 Hours

Next up, every MLO is required to complete 2 hours focused on Ethics. This module goes beyond just rules on a page; it dives into the real-world gray areas and dilemmas you might actually face. It’s all about reinforcing the high ethical bar set for professionals in the financial services industry.

The curriculum often uses case studies and practical scenarios that touch on fraud prevention, consumer protection, and fair lending. The goal isn’t just to tell you what’s right or wrong, but to train your professional judgment so you can spot ethical red flags and protect both your clients and your reputation.

Exploring Non-Traditional Mortgage Products: 2 Hours

The final core piece is 2 hours of training on non-traditional mortgage products. The lending landscape is anything but static. New and varied loan options are always emerging to meet the needs of a wider range of borrowers, and this section makes sure you’re not left behind.

Knowing these products inside and out makes you a far more valuable resource for your clients. You’ll be able to confidently discuss different lending solutions, which expands your ability to help more people in today’s diverse market.

When you break the 8-hour requirement down into these distinct parts—Federal Law, Ethics, and Non-Traditional Products—it’s clear that this is a practical, logical update designed to reinforce your expertise and keep you at the top of your game.

It’s also worth noting that the final hour is typically an elective, allowing you to focus on topics relevant to your specific market or interests. By completing a comprehensive online course, you can knock out all these requirements and get set for another successful year.

Finding the right educational partner makes meeting your mortgage continuing education goals a simple, straightforward process. Pending NMLS Approval each year, you can explore a variety of flexible online courses on our MLO Continuing Education page.

Navigating State-Specific CE Requirements

While the 8-hour NMLS course is the national standard for mortgage continuing education, think of it as just the starting point. It’s the foundation you build on each year. Many states add their own specific CE requirements on top of this, which can create a tricky compliance puzzle, especially if you’re licensed in more than one state.

These extra state-specific hours aren’t just busywork. They’re designed to cover unique local laws and market conditions that a broad federal course can’t possibly get into. A state might require an extra hour on its foreclosure process, specific anti-predatory lending rules, or recent tax changes affecting mortgages. This ensures you’re not just federally compliant but a true expert in the community you serve.

Why Do States Add Extra Hours?

Every state has its own legislative quirks and consumer protection priorities, and these are reflected in their CE rules. For instance, a state with a large retirement community might mandate an hour on reverse mortgages. Another, experiencing a construction boom, might focus on builder-affiliated lending.

The most important thing to remember is that these requirements are always changing. New laws get passed, and market trends shift. That’s why you absolutely must check the exact CE requirements for each state you’re licensed in, every single year, before you even think about starting a course.

Simply finishing the standard 8-hour course doesn’t mean you’re in the clear. Missing even one hour of a state-specific requirement can put your license at risk, even if you’ve met all your federal obligations.

The Challenge of Multi-State Licensing

For MLOs licensed in several states, keeping track of these different requirements takes some real planning. You might need one extra hour for Florida, two for California, and a specific topic for New York—all in addition to the core 8-hour federal mandate. Juggling all these moving parts can feel like a headache, but with the right strategy, it’s completely manageable.

One critical detail to keep in mind is the NMLS “Successive Years” rule. This rule prevents you from taking the exact same course two years in a row. So, that 9-hour “Florida + Federal” course you took last year? You can’t take it again this year, even if it’s been updated. You have to pick a course with a different NMLS course ID number.

Your Strategy for Seamless Compliance

Staying on top of your state-specific mortgage continuing education is pretty straightforward if you have a system. Your first move should always be to check the NMLS website for the latest requirements for every single one of your licenses. Make that your go-to source of truth.

To make life easier, many MLOs opt for course bundles that package federal and state requirements together. It’s an efficient way to make sure all your bases are covered. MLOs getting licensed for the first time, can find a detailed guide on what each state demands for pre-license education, you can explore comprehensive resources on state licensing requirements.

Ultimately, being proactive and organized is your best defense against compliance headaches. By confirming what you need early on and choosing the right courses, you can turn your annual renewal into a smooth, stress-free part of your job. This diligence doesn’t just protect your licenses—it reinforces your reputation as a knowledgeable and trustworthy MLO in every market you serve.

How CE Builds a Stronger Mortgage Career

Let’s be honest, it’s easy to see your annual mortgage continuing education as just another checkbox on a long to-do list. But the MLOs who are truly crushing it have a different mindset. They see this requirement as a strategic advantage—a yearly investment in their own professional growth.

Think of it this way: the mortgage industry never sits still. Embracing this annual learning is what keeps you ahead of the curve, giving you a powerful edge over the competition. Staying on top of new loan products, tech, and market trends lets you serve a wider, more diverse range of clients.

Gaining a Competitive Edge with Up-to-Date Knowledge

Your yearly CE is a direct pipeline to the latest industry intelligence. When you’re the one who understands the ins and outs of new non-traditional mortgage products or how AI is shaking up the lending process, you become a go-to resource for your clients. This is the kind of knowledge that helps you find creative solutions for borrowers who don’t fit the standard cookie-cutter mold.

This is especially true when you’re working with the next wave of homebuyers. First-time buyers are a huge, influential force in today’s market. In fact, according to the May 2025 ICE Mortgage Monitor, these buyers hit a record share of agency purchase lending in the first quarter of 2025. Individuals aged 35 and under accounted for over 50% of financed home purchases.

And it’s not just millennials. The report also pointed out that Gen Z buyers—those aged 18 to 27—were behind one in four of those first-time buyer loans. You can get a deeper dive into these numbers in the full ICE Mortgage Monitor report.

By staying current through your mortgage continuing education, you position yourself to confidently serve this growing client base, understand their unique challenges, and guide them to the closing table successfully.

This specialized knowledge isn’t just theory; it translates directly into more closed loans and a rock-solid reputation. When you can field complex questions with confidence, you build the kind of trust that fuels referrals and repeat business for years to come.

Mitigating Risk and Protecting Your License

Beyond just growing your business, continuing education is your best defense against risk. The regulatory landscape is a minefield of complex rules and frequent updates from agencies like the CFPB. Staying on top of the latest compliance pitfalls is absolutely essential for protecting yourself, your clients, and your employer.

Your CE courses drill down into the stuff that really matters, like:

- Fair Lending Practices: Knowing how to avoid discriminatory practices.

- Fraud Detection: Spotting the red flags in loan applications and documents.

- Disclosure Requirements: Making sure your clients get accurate and timely info.

A single compliance slip-up can lead to huge financial penalties and serious damage to your reputation. By dedicating time to your education, you’re actively lowering those risks and reinforcing your commitment to ethical lending.

From Obligation to Opportunity

When you start seeing your annual CE as a tool for advancement, everything changes. It’s no longer a chore, but an opportunity to sharpen your skills, grow your expertise, and become more valuable in a dynamic industry. The path from getting your first license to becoming a seasoned pro is paved with continuous learning. If you’re just starting out, our guide on how to become a mortgage loan originator lays out the entire career path.

For experienced MLOs, every renewal cycle is a chance to build on that foundation. When you truly engage with the material, you’re not just checking a box—you’re investing in a more resilient and successful career. Prioritizing your mortgage continuing education is one of the smartest business moves you can make each year.

Your Step-By-Step Plan to Complete CE

Let’s be honest, completing your annual mortgage continuing education can feel like one more thing on an already packed to-do list. But with a simple, straightforward plan, you can knock it out smoothly and make sure your license renewal is totally stress-free.

This roadmap breaks the whole thing down into easy, manageable steps. No jargon, no confusion—just what you need to do.

The trick is to get ahead of it. Waiting until the last minute is a recipe for stress and can even put your license at risk. If you start early and follow these steps, this yearly requirement becomes just another routine part of being a pro.

Step 1: Verify Your Specific Requirements with the NMLS

Before you even think about buying a course, your first move is to find out exactly what you need. The standard is the 8-hour NMLS course, but plenty of states have their own additional requirements.

And here’s a pro tip: never assume this year’s rules are the same as last year’s. They change. Log in to your NMLS account to get the official word for every state you’re licensed in. This is the only source that matters.

- Check Each State License: Look up the CE requirements for every single state license you hold. Don’t skip any.

- Note Specific Topics: Some states get very specific, requiring hours on topics like state law or fair lending. Jot these down.

- Confirm Total Hours: Add up the federal 8 hours plus all your state-specific hours to get your grand total for the year.

This literally takes five minutes, but it can save you from a massive headache later. Taking the wrong course or coming up short on hours is a nightmare you don’t need.

Step 2: Select the Right Online Courses

Okay, now that you know what you need, it’s time to pick your courses. Online education is a game-changer here, giving you the freedom to get this done from your office or your couch. No need to disrupt your entire week.

When you’re looking for a provider, make sure their courses are fully approved by the NMLS. This is the only way to keep your knowledge sharp and reinforce what you’re learning.

A great educational provider simplifies the renewal process. They should offer clear course descriptions, easy navigation, and transparent reporting to the NMLS, making the entire experience feel effortless.

Choosing a solid online self-paced option puts you in the driver’s seat. You can complete the modules whenever it works for you, turning a chore into a manageable part of your professional growth.

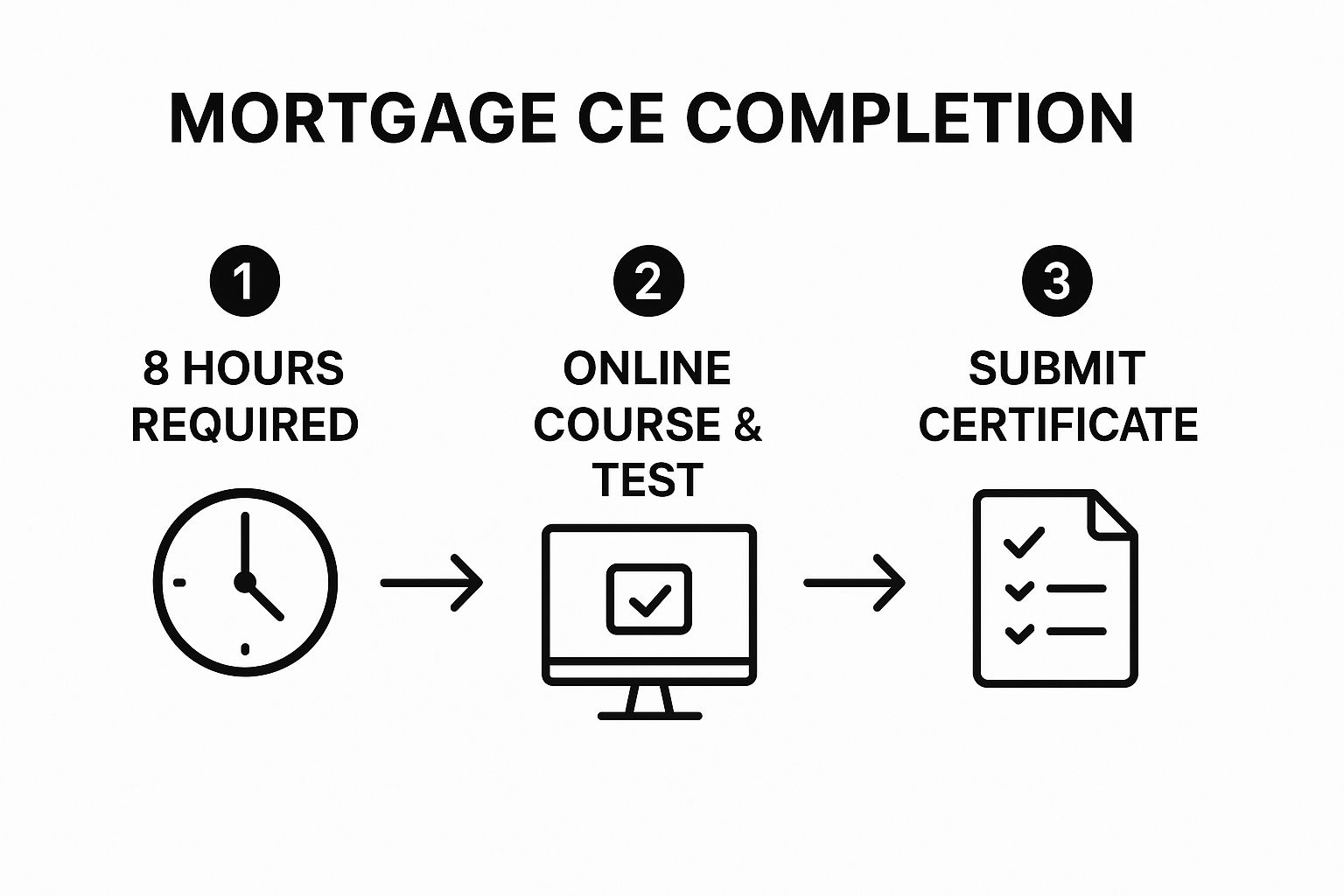

This infographic breaks down the core journey of getting the annual CE done for most of the USA.

As you can see, it’s a simple flow: figure out what you need, complete the course, and get it submitted.

Step 3: Complete the Coursework and Quizzes

Once you’re enrolled, it’s time to dive in. The courses are usually split into modules covering topics like federal law, ethics, and non-traditional mortgages. The system will have built-in checks, like Bio-Sig-ID, to make sure you’re actively participating—it’s an NMLS rule.

You’ll find short quizzes after each section to check your understanding. They aren’t there to trick you; they just make sure you’ve absorbed the key points before you continue. Passing them is how you move forward and earn your credit hours.

Step 4: Confirm Your Credits Are Reported

This is the final, and maybe most important, step. You’ve done the work, now you need to make sure you get credit for it. After you pass, your education provider reports your completed hours directly to the NMLS, within seven calendar days maximum, but typically within a day.

But don’t just assume it’s done. Log back into your NMLS account and see for yourself that the credits are posted. This is why you don’t wait until the last minute! Finishing early gives you a nice cushion for everything to get reported and verified properly.

Seeing those completed hours pop up on your NMLS record is the green light. You’re officially good to renew for another year. If you’re ready to get started, you can check to see if our current online MLO CE options are available for this year’s renewal.

Common Questions About Mortgage CE

When you’re juggling clients and closings, keeping up with mortgage continuing education can feel like one more thing on a never-ending to-do list. It’s totally normal to have questions, especially with renewal deadlines looming.

Let’s cut through the confusion. Here are straightforward answers to some of the most common questions MLOs ask about their annual CE.

What Happens If I Miss the MLO License Renewal Deadline?

Missing your CE deadline is a big deal. If you don’t complete your required hours by your state’s cutoff (usually December 31st), your NMLS license won’t be renewed. Plain and simple, that means you’re legally prohibited from originating loans. Your business grinds to a halt.

To get back in good standing, you’ll most likely have to take “Late CE” courses (if your state allows Late CE) specific to the year you missed. Expect to pay extra fees and navigate a more complicated reinstatement process. The best advice? Finish your education well ahead of schedule to avoid any disruption to your career.

How Do I Handle CE for Multiple State Licenses?

If you’re licensed in more than one state, you need to satisfy the CE requirements for every single one. The foundation is always the core 8-hour NMLS course that everyone takes. After that, it’s on you to figure out the state-specific hours needed for each license you hold.

The NMLS website is your best friend here—it has a detailed breakdown for every state. A little planning goes a long way. This ensures you can renew all of your licenses smoothly, without any last-minute surprises.

The secret to managing multiple state licenses is to start early. Make a simple checklist of your federal and state-specific hours, then find a course bundle that knocks everything out in one shot.

This simple habit saves a ton of stress and keeps you compliant across all the markets you serve.

Can I Take the Same CE Course Two Years in a Row?

Absolutely not. The NMLS has a strict “Successive Years” rule that prevents MLOs from taking the same CE course two years running. This rule exists for a good reason: it ensures you’re always learning about the latest industry changes and not just rehashing old material.

Education providers create brand-new courses every single year to comply with this mandate. When you’re picking a course, double-check that it’s approved for the current renewal year. It’s a small step that prevents major headaches with getting your credits accepted by the NMLS.

How Are My Completed CE Hours Reported to the NMLS?

Once you finish your NMLS-approved course, the good news is that reporting is not your job. Your education provider electronically submits your completion record to the NMLS, typically within seven calendar days. Make sure they have the correct spelling of your last name in your NMLS account and your NMLS ID number. These must match, or your hours cannot be reported.

Even so, it’s smart to be proactive. A few days after you finish, log into your NMLS account and personally confirm that your credits have posted correctly.

Once you are logged in, hit “COMPOSITE VIEW” in the upper right hand corner of your screen, then hit “VIEW INDIVIDUAL” (top of screen) Next hit educational record (left side of screen) and scroll to where you see CE Education listed.

Finishing your courses early gives everyone plenty of time for reporting and verification, giving you complete peace of mind.

At 24hourEDU, we make it easy to fulfill your annual educational requirements. Our fully online education includes our support, giving you the tools you need to succeed. Find the right course for your renewal at our MLO Continuing Education page.