When you're deciding where to hang your MLO license, the choice between a mortgage broker and a bank lender really comes down to one thing: variety versus simplicity.

Think of a mortgage broker as a personal shopper for loans. They have access to dozens of lenders and can hunt down the best possible deal for a client. On the other hand, a bank lender works for a single institution and offers only its in-house loan products. It's a direct, one-stop-shop experience.

Breaking Down the Core Differences

Getting a handle on the mortgage broker vs. bank lender dynamic is the first critical step for any aspiring Mortgage Loan Originator (MLO). It's also fundamental for homebuyers trying to navigate their options.

Brokers generally have a much wider arsenal of loan products, making them a great fit for clients with unique financial situations. Banks tend to offer a more straightforward process, which works well for customers with conventional borrowing needs. This initial choice you make as an MLO will shape everything from the interest rates you can offer to how quickly you can get a deal to the closing table.

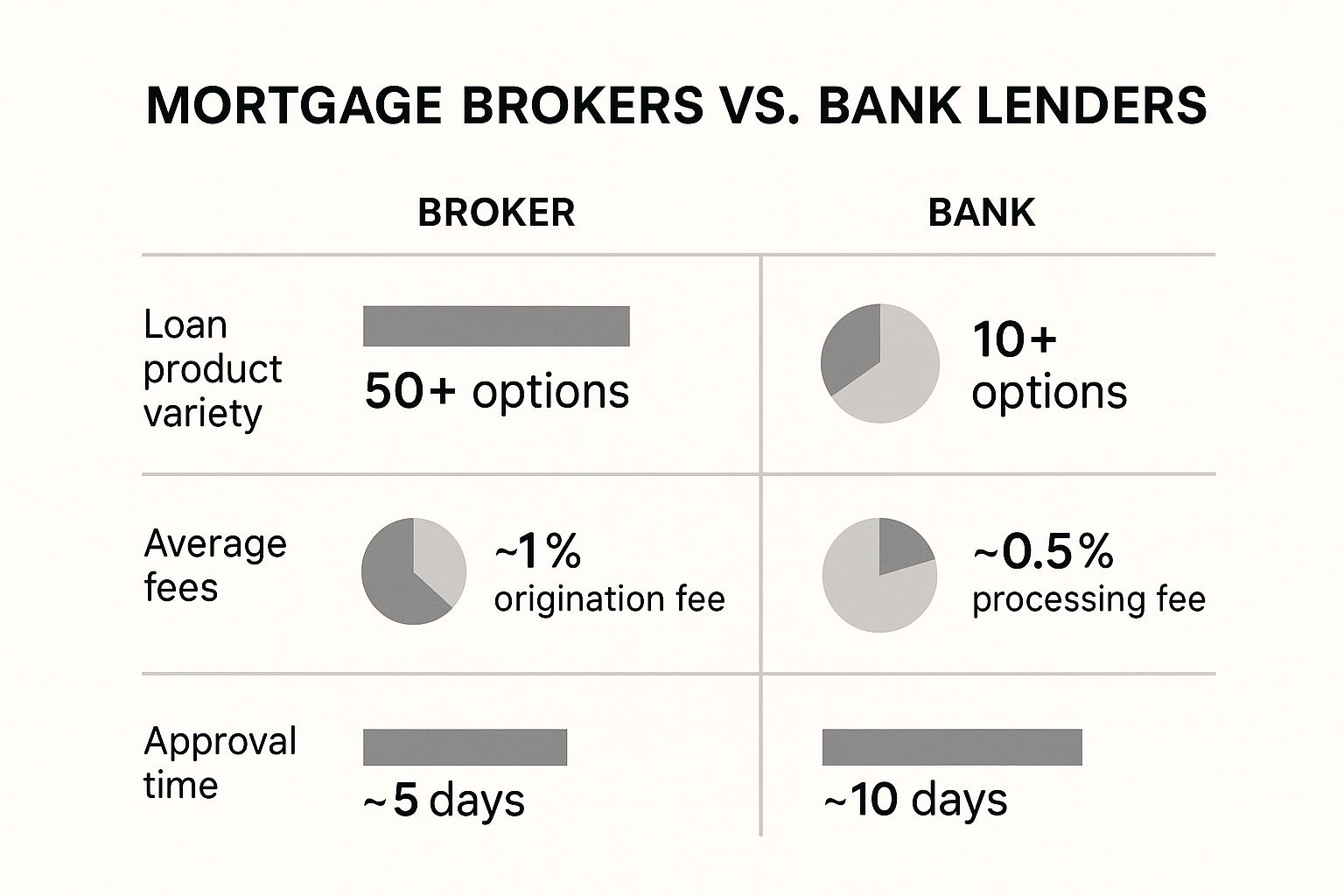

This infographic breaks down some of the key differences in product variety, typical fees, and how fast you can expect approvals.

As you can see, brokers often have access to far more loan options and can sometimes get approvals faster, though their fee structures can differ from banks.

To really spell it out, here’s a side-by-side look at how their service models and ideal clients stack up.

Core Differences: Broker vs. Bank

The table below provides a quick, at-a-glance comparison of the two career paths, highlighting their distinct service models, product offerings, and the types of borrowers they are best equipped to serve.

| Criteria | Mortgage Broker | Bank Lender |

|---|---|---|

| Service Model | Acts as an intermediary, shopping for loans across a network of wholesale lenders. | Works for a single financial institution, offering only their in-house mortgage products. |

| Loan Variety | High; access to diverse loan types (FHA, VA, jumbo, non-QM) from multiple sources. | Limited; offers only the bank's proprietary loan portfolio and standard conventional loans. |

| Best For | Borrowers with unique financial profiles, self-employed individuals, or those seeking the best rate. | Customers with strong credit, straightforward finances, and an existing relationship with the bank. |

Ultimately, understanding these distinctions is key to deciding which environment best suits your skills and career goals as a loan originator.

How Mortgage Brokers and Bank Lenders Work

To really get to the heart of the mortgage broker vs bank lender debate, you first need to understand their completely different ways of operating. Think of a mortgage broker as a professional matchmaker. They're the go-between, connecting you (the borrower) with a whole network of wholesale lenders. They don't actually fund the loan themselves; instead, they take your application and shop it around to find you the best deal.

A bank lender, on the other hand, works directly for one institution, like a bank or credit union. Their job is to sell and process loans using only the products their specific employer offers. This makes for a more straightforward path, but it also means you're limited to a much smaller menu of loan options.

The Broker Workflow: A Flexible Approach

A mortgage broker's process starts with a deep dive into your financial situation—credit, income, debts—to figure out exactly what you need. From there, they take your single application and send it out to multiple lenders, from big national banks to smaller, specialized finance companies. This process naturally creates competition for your business, which often leads to better rates and terms for you.

And it’s an approach that's clearly catching on. In the fourth quarter of 2023, mortgage brokers handled 24.3% of the U.S. mortgage market, which is their highest share since way back in 2009. This growth shows that more and more borrowers are putting their trust in the independent model.

The image below gives you a clear visual of how these relationships work in the brokerage world.

As you can see, the broker is the central hub, managing the connection between the borrower and the lender without ever directly funding the loan themselves.

The Bank Lender Process: A Direct Path

When you work with a bank lender, you're applying right at the source of the money. A loan officer at a bank will walk you through their own institution's specific application process and underwriting rules. While this direct route can feel simpler, it locks you into one set of guidelines and one portfolio of loan products.

For anyone looking to become an MLO, understanding the subtle but critical differences between a bank's loan officer and an independent broker is key. You can check out a deeper dive into these roles in our guide on the loan officer vs mortgage broker comparison. Getting this distinction right is a fundamental first step in your career.

Analyzing Current Market Share and Trends

The battle between mortgage brokers vs bank lenders isn't a static one. It’s constantly shifting, shaped by the economy and what borrowers are looking for. Over the last decade, we've seen a clear trend: business is steadily moving away from big banks and flowing directly to non-bank lenders, a group where mortgage brokers are major players.

This isn't just a small market correction, either. Non-bank mortgage companies now handle more than half of all home loans in the country. In 2023, they were behind a massive 53.3% of total home loan originations. That’s a huge jump from just 44.6% in 2018.

Over that same five-year stretch, traditional banks saw their slice of the pie shrink from 42.5% all the way down to 30.1%.

Why Are More Borrowers Choosing Brokers?

So, what's causing this massive shift? A huge piece of the puzzle is the flexibility and sheer variety of loan products brokers can offer. After the 2008 financial crisis, many banks slammed the door shut with incredibly tight lending rules, making it tough for anyone with less-than-perfect credit or a non-traditional income to get approved.

Brokers stepped right into that gap. With access to a whole network of lending partners, they can find a home for loans that a single bank, with its rigid underwriting box, would instantly deny.

For an aspiring Mortgage Loan Originator, this trend is a massive flashing green light. The explosive growth in the non-bank sector points to a thriving career field where skilled MLOs who can navigate a diverse menu of loan products are in serious demand.

This movement highlights a real change in how people think about getting a mortgage. They're actively seeking out the personalized touch and wider range of options that brokers bring to the table. For anyone thinking about jumping into this career, the first step is understanding the mortgage broker license requirements. It's a path full of opportunity, giving you the chance to build a business around helping clients find the perfect fit.

Comparing Loan Costs and Potential Savings

When you’re weighing a mortgage broker vs bank lender, it all comes down to the bottom line: cost. It might seem like going directly to a bank would be cheaper, but the reality is way more nuanced. How each one gets paid has a massive impact on the total cost of the loan, from the fees you pay upfront to the interest you’ll be shelling out for years.

A bank lender’s costs are all wrapped up in their own loan products. This means their origination fees, processing fees, and the interest rate are all set by one institution. Their pricing is what it is, locked within their own ecosystem.

A mortgage broker, on the other hand, is compensated by the wholesale lender they place your loan with. This dynamic naturally creates a competitive battlefield. Lenders have to offer sharp rates and lower fees to win the broker's business, and those savings get passed directly to the borrower.

Understanding Fee Structures

The real secret lies in the wholesale pricing that brokers get access to. Banks offer retail rates to the general public, but brokers are tapping into a completely different pricing tier—one you can't get by just walking into a branch. This access lets them shop your loan to find the best possible combination of interest rates and closing costs.

Think about it this way: a bank might quote you a single rate of 6.5% with a $1,500 origination fee. A broker, however, can put that loan out to bid with ten different lenders. They might find one offering 6.25% with a similar fee, or another at 6.5% with no origination fee at all. You get choices.

This is a look at the portal for Home Mortgage Disclosure Act (HMDA) data from the Consumer Financial Protection Bureau. It’s a goldmine of information for analyzing lending trends and costs across the entire industry.

This kind of data is what uncovers the real-world savings and lets us compare how lenders are actually performing on a national scale. It brings a level of transparency to the market that empowers everyone, from MLOs to the consumers they serve.

The Impact on Lifetime Savings

Over the 30-year life of a mortgage, even a tiny difference in the interest rate can add up to thousands upon thousands of dollars. The ability to shop the market is a broker’s single greatest weapon for their clients.

The proof is in the numbers. A deep dive into recent mortgage data shows just how much this competition can save a borrower over the long haul.

| Channel | Average Savings Per Loan |

|---|---|

| Independent Mortgage Broker | $10,662 |

This data confirms that the ability to compare multiple loan options really does translate to significant, tangible savings.

A recent analysis of 2023 HMDA data revealed that borrowers who worked with an independent mortgage broker saved an average of $10,662 over the life of their loan compared to those using retail lenders. This highlights the real financial benefit of having a professional compare multiple loan options on your behalf. You can learn more about these findings on how brokers benefit borrowers' wallets.

This shows that while fees are definitely part of the conversation, the long-term savings from locking in a lower interest rate often make the biggest difference in the mortgage broker vs bank lender debate.

Choosing the Right Path for Your Situation

Figuring out whether to go with a mortgage broker vs bank lender isn't about finding a single "best" option. The right choice really comes down to the borrower's specific situation. There’s no universal answer—it all depends on their financial picture, the property they’re after, and how they feel about the whole process.

For any aspiring Mortgage Loan Originator, this is where you prove your worth. Understanding these differences is what separates a decent MLO from a truly great one. Your career will be built on your ability to steer clients toward the channel that actually serves their needs.

When a Bank Lender Makes More Sense

For borrowers with a clean, straightforward financial profile, a bank lender is often the path of least resistance. If you've got a solid W-2 job history, great credit, and a healthy down payment, the bank's direct process is hard to beat for efficiency. Their in-house underwriting is practically built for conventional loan files like these.

A bank is probably the better fit in these cases:

- Existing Relationships: If you already bank somewhere, you might get access to relationship discounts or special pricing. It pays to ask.

- Jumbo Loans: Big banks often keep jumbo loans on their own books instead of selling them. This can give them more wiggle room on rates and terms for those high-dollar properties.

- A Need for Simplicity: Some people just feel more comfortable working with a well-known brand. The direct-to-lender experience a bank offers feels safer and less complicated for many first-time buyers.

For a new MLO, a bank provides a fantastic learning environment. You get a steady stream of leads from the bank’s existing customer base and a structured system to learn the fundamentals of lending inside and out.

Why a Mortgage Broker Often Has the Edge

Mortgage brokers really come into their own when things get complicated. Their superpower is their access to a huge network of lenders, which means they can find a home for loans that a single bank would flat-out deny.

A broker is almost always the better choice when:

- Complex Income: If you're self-employed, work on commission, or have a freelance gig, a broker knows which lenders are comfortable with non-traditional income.

- Credit Challenges: For borrowers with a few bumps on their credit report, a broker can shop the loan to lenders who specialize in FHA loans or other programs with more forgiving requirements.

- Niche Loan Products: Need a non-QM loan, a bank statement program, or financing for a unique property? A broker's network is the best place to find a lender who will take on that kind of deal.

For an MLO, working at a brokerage is the entrepreneurial route. It gives you the freedom to build your personal brand and serve a much wider range of clients by offering creative solutions that most banks just can't touch.

How to Get Your MLO License for Either Path

Whether you’re drawn to the structured environment of a bank or the entrepreneurial hustle of a brokerage, your journey begins at the exact same starting line: getting your Mortgage Loan Originator (MLO) license.

This isn't a recommendation; it's a requirement. The path to becoming an MLO is regulated by the Nationwide Multi State Licensing System and Registry (NMLS), which sets the educational bar for the entire industry. This ensures that every MLO, no matter where they hang their shingle, has the essential knowledge to serve borrowers ethically and competently.

The cornerstone of this requirement is completing 20 hours of NMLS-approved pre-licensing education. This isn't just about checking a box—this coursework dives deep into federal laws, ethics, and lending standards that are crucial for success in either a broker or bank lender role.

We Make the Education Path Easy

Getting your MLO license is an easy and straightforward process with our help. That’s why our education is fully online, letting you knock out the required training quickly. Better yet, our comprehensive package includes our exam prep package for free, because we want you to have the confidence to pass the SAFE MLO test on your first try.

Here’s what the process boils down to:

- Complete the 20-Hour SAFE Course: Our NMLS-approved course fulfills the national requirement.

- Pass the SAFE MLO Test: This exam will test you on everything you learned in your pre-licensing education.

- Apply for Your License: You'll submit your official application through the NMLS.

We believe starting your career should be straightforward. Choosing the right program is the first step, and we've built ours to give you everything you need to succeed.

The most important decision you'll make at the start of your journey is selecting an education provider that prepares you for the realities of the job. Our courses are fully approved by the NMLS Nationwide Multi State Licensing System and Registry, ensuring you meet all national standards for becoming a licensed professional.

From start to finish, we’re here to support your goals. Understanding how to choose the right mortgage licensing program is a crucial first step, and our goal is to make that choice an easy one. With our online platform, you can quickly complete your education and move confidently toward your new career in the mortgage industry.

Got Questions? We've Got Answers

When you're weighing a career as a mortgage broker vs. a bank lender, a few key questions always come up. Let's tackle them head-on so you can move forward with a clear picture, whether you're just curious or an aspiring MLO ready to jump in.

Is It Faster to Get a Loan from a Bank or a Mortgage Broker?

This really depends on the borrower's situation. If you have a straightforward financial profile and a long-standing relationship with your bank, they can often move things along pretty quickly. Their internal process is built for conventional, low-complexity loans.

But when things get complicated, a mortgage broker often pulls ahead. They're masters at navigating tricky files and know exactly which wholesale lenders specialize in fast turnarounds for unique situations. For a non-traditional borrower, a broker can actually shave significant time off the process.

Are Mortgage Broker Fees Higher Than a Bank's?

Not always. It's a common misconception. While brokers do earn a commission (usually paid by the wholesale lender, not the borrower), their real power comes from shopping the market. They can pit dozens of lenders against each other to find the best rate, which can lead to a much lower overall cost for the borrower.

You have to look at the total value, not just one fee. A bank's costs are simply baked into the single loan product they offer. The only way to know for sure is to compare the official Loan Estimate from both a broker and a bank—that's where the true costs are laid bare.

Which MLO Career Path Is Better for a New Agent?

Honestly, there's no single "better" path. It comes down to your personality and career goals.

Starting at a bank gives you the power of a recognized brand and a structured environment. You'll likely get a steady stream of leads handed to you, making it a fantastic place to learn the fundamentals without the pressure of building a business from scratch.

On the flip side, a brokerage offers freedom. You get more flexibility, a higher potential commission ceiling, and the thrill of building your own brand. It’s entrepreneurial to its core. Our NMLS-approved licensing education, packed with insights from industry veterans, is designed to set you up for success no matter which environment you choose.

Ready to kickstart your journey in the mortgage industry? 24hourEDU makes getting your MLO license simple and straightforward. Our fully online, NMLS-approved education includes everything you need, including our exam prep package for free. Enroll today and take the first step toward your new career at https://24houredu.com.