Your Home Buying Team: Mortgage Broker vs Real Estate Broker

A successful home purchase almost always involves a team of experts, and knowing who does what is the first step. Though both are called “brokers,” their roles couldn’t be more distinct. One professional is focused entirely on the physical property, while the other is your expert for securing the financing.

A real estate broker is your guide through the property market itself. They’re licensed pros who help you pinpoint homes that fit your wish list, negotiate with sellers to get you the best price, and manage all the complicated paperwork that comes with transferring ownership. Their main job is to get you the keys to the right house on the best possible terms.

On the other hand, a mortgage broker is your financing specialist. These professionals are licensed Mortgage Loan Originators (MLOs) whose job is to take your financial profile and shop it around to a whole network of different lenders. Their goal is to find you the most competitive interest rate and loan terms available, acting as the crucial middleman between you and the banks.

Distinguishing Their Core Functions

To put it simply, you can’t really have one without the other in a typical home purchase. The real estate broker helps you win the house, and the mortgage broker makes sure you can actually afford it.

The table below breaks down their fundamental differences at a glance.

At a Glance: Mortgage Broker vs Real Estate Broker

| Aspect | Mortgage Broker | Real Estate Broker |

|---|---|---|

| Primary Focus | Securing the best loan and financing for you, the buyer. | Finding and negotiating the purchase of the physical property. |

| Represents | You (the borrower) to a network of different lenders. | You (the buyer or seller) in the property transaction itself. |

| Area of Expertise | Loan products, interest rates, credit analysis, and underwriting. | Local market conditions, property valuation, and contract negotiation. |

This quick comparison makes it clear: while they work in parallel, their expertise and responsibilities are in completely separate fields.

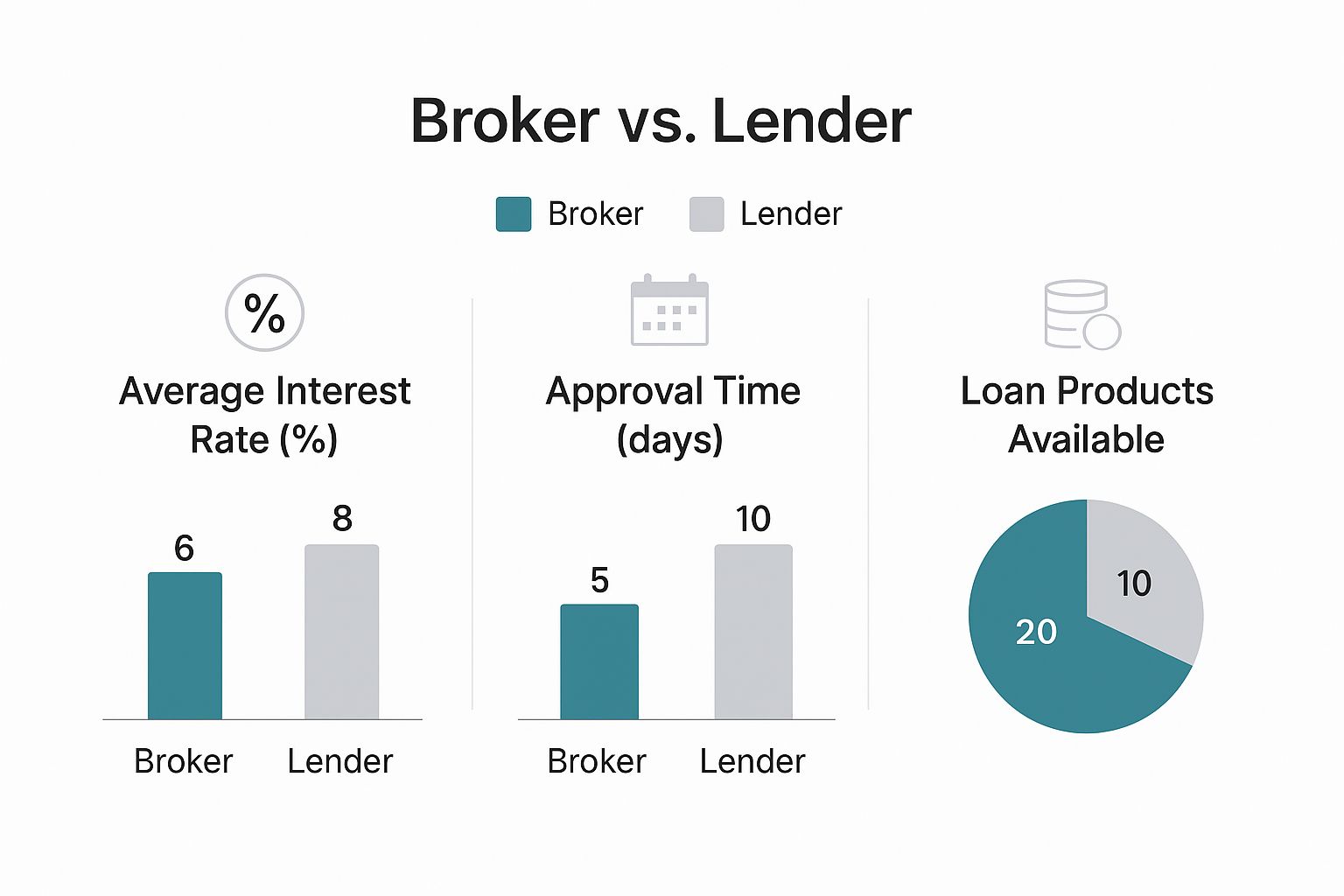

The chart below shows just how much impact a broker’s wider access to the market can have on critical factors like interest rates and the sheer number of loan options available to you.

As the data shows, working with a professional who can shop around on your behalf often leads to much more competitive options. It’s about leveraging their network to save you money in the long run.

Breaking Down Their Core Responsibilities

While both mortgage and real estate brokers are your guides in the home-buying journey, they operate in completely different worlds. Think of it this way: one is focused on the physical property—the house itself—while the other handles the complex financial deal needed to actually buy it. Once you understand their specific duties, it’s easy to see why you need both experts in your corner.

The Real Estate Broker’s Domain

Your real estate broker is the property expert. Their entire world revolves around houses, neighborhoods, and the local market. They’re the ones on the ground with you, handling everything from finding potential homes to getting that final purchase agreement signed.

Here’s a look at their primary duties:

- Market Analysis: They dig into neighborhood values, recent sales, and market trends to help you put together a smart, informed offer.

- Property Showings: Your broker is the one scheduling and walking you through homes, pointing out key features and potential red flags you might otherwise miss.

- Offer Strategy and Negotiation: This is where they really shine. They help you craft a competitive offer and go to bat for you, negotiating with the seller’s agent on price, contingencies, and closing dates to get you the best possible deal.

- Contract Management: They manage all the complicated paperwork, from the initial offer to the final closing documents, ensuring the whole transaction is smooth and legally sound.

The Mortgage Broker’s Focus

A mortgage broker, on the other hand, is your financial strategist. Their job starts with a deep dive into your finances to figure out exactly how much you can borrow. They act as your champion in the lending world, fighting to find the money you need on the best possible terms.

A mortgage broker’s primary allegiance is to you, the borrower. Their job is to navigate the complex lending landscape and find a loan that aligns perfectly with your financial situation, not just push a single bank’s product.

Their key responsibilities look quite different:

- Financial Assessment: They analyze your income, assets, debt, and credit history to get a clear picture of what loan programs you’ll qualify for.

- Loan Shopping: A mortgage broker takes your single application and shops it around to multiple lenders—banks, credit unions, and wholesale lenders—to find the most competitive rates and terms.

- Application Guidance: They help you put together a clean, accurate loan application, making sure all your documentation is in order to make you look like a strong candidate to underwriters.

- Navigating Underwriting: The broker is your go-between with the lender’s underwriting department. They help clear up any questions or conditions that pop up during the approval process.

While their roles are distinct, it’s also helpful to know how a mortgage broker differs from a loan officer. For a closer look, you can explore the key differences between a loan officer and a mortgage broker in our detailed guide: https://24houredu.com/loan-officer-vs-mortgage-broker/

How Each Professional Gets Compensated

It’s smart to know how your mortgage broker and real estate broker get paid. Why? Because their paychecks are tied directly to their roles in your home purchase, and understanding this helps clarify everyone’s incentives. While both typically get paid when the deal closes, where the money comes from and how it’s structured are completely different.

Real Estate Broker Commissions

A real estate broker’s pay comes from a commission, which is simply a percentage of the home’s final sale price. This rate isn’t set in stone—it’s negotiable—but it usually lands somewhere in the 5-6% range. The interesting part is who foots the bill.

In almost every case, the seller pays the entire commission out of their proceeds from the sale. That single commission is then split between the seller’s broker and the buyer’s broker, who then pay their own agents.

For a buyer, this means you generally do not pay your real estate broker’s commission out of your own pocket. Their fee is essentially built into the home’s sale price and paid by the seller.

Mortgage Broker Compensation Models

A mortgage broker’s compensation is linked directly to the loan they arrange for you. Thanks to federal regulations from the Dodd-Frank Act, brokers can’t get paid by both you and the lender for the same loan, which keeps potential conflicts of interest in check. This leaves two main ways they get paid.

- Lender-Paid Compensation (LPC): This is the most common setup by far. The lender who provides your loan pays the mortgage broker a fee, sometimes called a yield-spread premium. It’s calculated as a percentage of your loan amount, but it’s not a separate line item you have to pay at closing. Instead, it’s indirectly baked into the interest rate you’re offered.

- Borrower-Paid Compensation: With this option, you pay the mortgage broker a fee directly. It’s typically a percentage of the loan amount (like 1%) and shows up in your closing costs. The upside? This can sometimes land you a lower interest rate from the lender, since they aren’t the ones paying the broker’s fee.

Getting a handle on these payment structures is a big part of the broker vs. lender decision. It gives you the confidence to ask direct questions about how your pros are getting paid, ensuring everything is crystal clear as you move forward.

The Path to Professional Licensing

You can’t just hang a shingle and start brokering deals in the mortgage or real estate world. Both professions are built on a foundation of trust and verified expertise, which is why they operate in highly regulated industries.

Before anyone can guide you through a major financial decision, they must meet tough, state-specific licensing and education standards. It’s all about consumer protection—ensuring the professional you hire has proven their competence.

For a real estate broker, this means completing extensive coursework covering the ins and outs of property law, contracts, and ethics before passing a challenging state exam. Their license is proof they can handle the legal complexities of transferring property.

Specialized Training for Mortgage Professionals

The path for a mortgage broker, officially known as a Mortgage Loan Originator (MLO), is largely standardized at the federal level. To earn a license, every MLO must be approved through the Nationwide Multistate Licensing System and Registry (NMLS).

This isn’t a simple weekend course. The process includes:

- Completing 20 hours of NMLS-approved pre-licensing education.

- Passing the national SAFE MLO Test with a score of 75% or higher.

- Undergoing a full criminal background check and credit check.

This structured training dives deep into federal law, ethics, and responsible lending practices, ensuring they are fully qualified to handle your sensitive financial information.

The rigorous NMLS approval process is what separates a professional MLO from an unverified advisor. It provides a layer of security and accountability, confirming your broker is held to the highest industry standards.

The demand for skilled mortgage professionals is undeniable. The global loan brokers market was valued at around $251 billion in 2021 and is projected to skyrocket, showing just how critical these experts have become. You can read the full research on the loan brokers market to see the numbers for yourself.

If you’re inspired by this high-income career path, getting started has never been more straightforward. Our fully approved online education makes earning your MLO license easy, and we even include our complete exam prep package for free to help you succeed. Find out more by reviewing our detailed guide on mortgage broker license requirements.

Who to Call First for a Strategic Advantage

When you’re starting the home-buying journey, there’s a specific order of operations that can give you a massive strategic advantage. It’s always tempting to dive right in and start looking at houses with a real estate broker, but the smartest play is to call a mortgage broker first. Think of it this way: getting your financing locked in is the foundation for your entire house hunt.

Lock In Your Budget Before You Shop

Talking with a mortgage professional right out of the gate gives you the single most important piece of information you’ll need: your budget. A mortgage pre-approval tells you exactly how much you can afford to spend. This simple step helps you avoid the all-too-common heartache of falling in love with a home that’s financially out of reach.

This crucial first step does a few powerful things for you:

- Sets a Realistic Price Range: It immediately narrows down your property search, making it far more efficient and focused.

- Strengthens Your Offer: A pre-approval letter signals to sellers that you’re a serious, qualified buyer, making your offer much more competitive.

- Speeds Up Closing: With your financing already arranged, the closing process can move forward much more quickly once you have an accepted offer.

Engaging a mortgage broker first transforms you from a casual house hunter into a powerful buyer. It positions your real estate broker for success by allowing them to negotiate on your behalf from a position of financial strength.

This initial consultation with a mortgage expert is your first and most important move. It sets the tone for a smoother, more successful home-buying experience by putting your financial power front and center. By handling the financing first, you’re not just shopping for a house; you’re making a calculated, confident investment. The debate over a mortgage broker vs bank lender is another key decision, but starting with a broker often provides the widest range of options from the get-go, giving you a strong start.

Mortgage Broker FAQs

1. What is the fundamental difference between a mortgage broker and a real estate broker?

A real estate broker helps you with the property itself—finding the right home, negotiating the price, and managing the purchase agreement. A mortgage broker helps you with the financing—finding the right loan, comparing lenders, and managing the mortgage application process.

2. Who does each broker represent?

A real estate broker (or their agent) represents you, the buyer or seller, in the property transaction. A mortgage broker acts as an intermediary, representing you, the borrower, to a network of different banks and lenders to find a suitable home loan.

3. What is the main goal of a real estate broker?

The primary goal of a real estate broker is to help their client successfully buy or sell a property at the best possible price and terms. They focus on the physical asset and the legal transfer of ownership.

4. What is the main goal of a mortgage broker?

A mortgage broker’s main objective is to secure the most favorable loan for their client. This includes finding the best available interest rate, loan terms, and lowest fees by shopping your application to various lenders.

5. How does a real estate broker get paid?

Real estate brokers are typically paid a commission, which is a percentage of the property’s sale price. This commission is usually paid by the seller from the proceeds of the sale and is split between the buyer’s and seller’s brokers.

6. How does a mortgage broker get paid?

Mortgage brokers are typically paid in one of two ways: through a lender-paid fee (a commission from the lending institution that funds the loan) or a borrower-paid fee (a percentage of the loan amount paid by the homebuyer at closing). Regulations prevent them from being paid by both on the same transaction.

7. Do I work with the mortgage broker or the real estate broker first?

While you can search for homes at any time, it’s highly recommended to speak with a mortgage broker or lender first. Getting pre-approved for a loan gives you a clear budget, strengthens your purchase offer, and shows sellers you are a serious buyer.

8. Is a real estate agent the same as a real estate broker?

Not exactly. A real estate agent is a licensed professional who must work under a licensed real estate broker. The broker has additional training and qualifications and is legally responsible for the transactions of the agents working for them. Many buyers and sellers will work directly with an agent.

9. Can one person be both a real estate broker and a mortgage broker?

Yes, an individual can hold licenses for both professions. However, it is often restricted and generally considered a conflict of interest for them to act as both your real estate agent and your mortgage broker on the same transaction due to disclosure requirements and potential ethical concerns.

10. What qualifications and licensing do they need?

Both professions require state licensing. Real estate brokers must complete specific coursework and pass a state exam. Mortgage brokers must also complete pre-licensing education and pass the national SAFE Mortgage Loan Originator Test, in addition to any state-specific requirements, and register with the Nationwide Multistate Licensing System (NMLS).

11. Who handles the property showings and open houses?

The real estate broker or their agent is responsible for all property-related activities, including finding homes that meet your criteria, scheduling tours, and showing you properties.

12. Who analyzes my credit report and financial documents?

The mortgage broker is the professional who will perform a deep dive into your finances. They will analyze your income, assets, debts, and credit history to determine which loan programs you qualify for.

13. Do I need a real estate broker to buy a house?

Legally, no. You can purchase a property without one, for instance, if you’re buying directly from a seller you know. However, an experienced real estate broker provides invaluable market knowledge, negotiation skills, and guidance through a complex legal process.

14. Do I need a mortgage broker to get a loan?

No. You can apply for a mortgage directly with a bank, credit union, or online lender. The advantage of a mortgage broker is that they do the shopping for you, potentially giving you access to more loan options and lenders than you could find on your own.

15. Who attends the closing with me?

Typically, your real estate agent will attend the closing to ensure the property transaction is completed smoothly. While your mortgage broker usually doesn’t attend the closing, they work behind the scenes with the lender and title company to make sure your loan documents are prepared and the funds are ready for the transaction.

Ready to start a high-income career as a Mortgage Loan Originator? At 24hourEDU, our fully NMLS-approved online education makes it easy to get your license. Our courses include our complete exam prep package for free, giving you everything you need to succeed. Get started today at 24houredu.com.