What Is Mortgage Origination Fee A Simple Guide for MLOs

Unlock what is mortgage origination fee, how it’s calculated, and its impact on APR. Essential knowledge and negotiation tips for aspiring MLOs.

On a $500,000 loan, a mortgage loan officer's gross commission typically lands somewhere between $2,500 and $5,000. This isn't just a job; it's a high-income career where your ambition directly fuels your paycheck, offering a clear path to financial success.

Becoming a Mortgage Loan Originator (MLO) is an exciting move into a field known for its significant earning potential. The freedom to work from home, name your own hours, and get paid based on your performance makes it a highly attractive career. Let's break down exactly how that compensation gets calculated.

The industry uses a standard called "basis points" (BPS) to figure out commission rates. Think of it as just a fancy way of talking about percentages. Loan officers typically earn between 0.50% to 1.00% of the total loan amount in commission.

Let's put that into perspective. At a pretty common rate of 0.75%, the gross commission on a $500,000 loan works out to be exactly $3,750. You can explore more about how MLO commission rates add up by checking out our comprehensive guide to loan officer income.

To make it even clearer, here’s a quick snapshot of what you could earn at different commission rates on that same $500,000 loan.

| Commission Rate (Basis Points) | Percentage | Gross Commission on $500,000 |

|---|---|---|

| 50 BPS | 0.50% | $2,500 |

| 75 BPS | 0.75% | $3,750 |

| 100 BPS | 1.00% | $5,000 |

| 125 BPS | 1.25% | $6,250 |

This table gives you a solid idea of the gross numbers, but it's just the starting point.

While the gross commission is straightforward, your actual take-home pay depends on a few important variables. Your experience level, the type of loan product you're selling, and—most importantly—your employer's commission split all play a role. These are the things that determine how much of that gross number ends up in your bank account after closing a deal.

A solid understanding of loan mechanics is essential for success. Getting comfortable with tools like the key Excel financial formulas for loan analysis can give you a strong foundation to build your career on.

This career allows you to directly control your income. The more you learn and the harder you work, the more you can earn—it's that simple.

Getting your MLO license is the first step, and our fully online, NMLS-approved education makes it easy. We even include our complete exam prep package for free to make sure you have everything you need to succeed.

To really get how loan officer commissions work, you have to get comfortable with one key term the entire industry runs on: basis points. It sounds a bit technical, but it’s actually incredibly simple. You'll hear it called BPS for short.

Think of it like this: one basis point is just one-hundredth of a single percent (0.01%). That's it. So, if your commission is 100 BPS, that’s just a straightforward 1.0% of the total loan amount.

Let’s plug that directly into our big question: how much commission does a loan officer make on a $500,000 loan?

So, a 100 BPS commission on a $500,000 loan gets you $5,000 in gross commission. This is the starting number before any splits with your brokerage or bank, which we’ll get into next.

Loan officers are usually paid in one of two ways, and the model often depends on where you hang your license.

Industry data from 2025 shows just how much those rates matter. On average, retail loan officers are seeing commissions between 92-103 basis points. On a $500,000 loan, that’s a gross commission of roughly $4,600 to $5,150. The real go-getters who crush their production goals can push that to 110 BPS or more, clearing $5,500 on a single deal. You can dig into the latest compensation analysis for a deeper dive into these numbers.

The beauty of a commission-based career is that your effort directly translates into income. By mastering the loan process and building your network, you can significantly increase your BPS rate over time.

This powerful income potential is exactly what draws so many people to the mortgage world. And getting started is easier than you think. Our completely online education is fully approved by the NMLS Nationwide Multi State Licensing System and Registry and designed to get you licensed and earning quickly. We even throw in our exam prep package for free, giving you every tool you need to succeed. This is your first step toward a high-earning career that you control.

So, you’ve calculated the gross commission based on basis points. That’s a great first step, but it's not the number that will show up in your bank account. The single biggest factor determining your actual take-home pay is your employer and their specific commission split.

Where you hang your license—whether at a traditional retail bank or an independent mortgage brokerage—will radically change what you earn on every single loan.

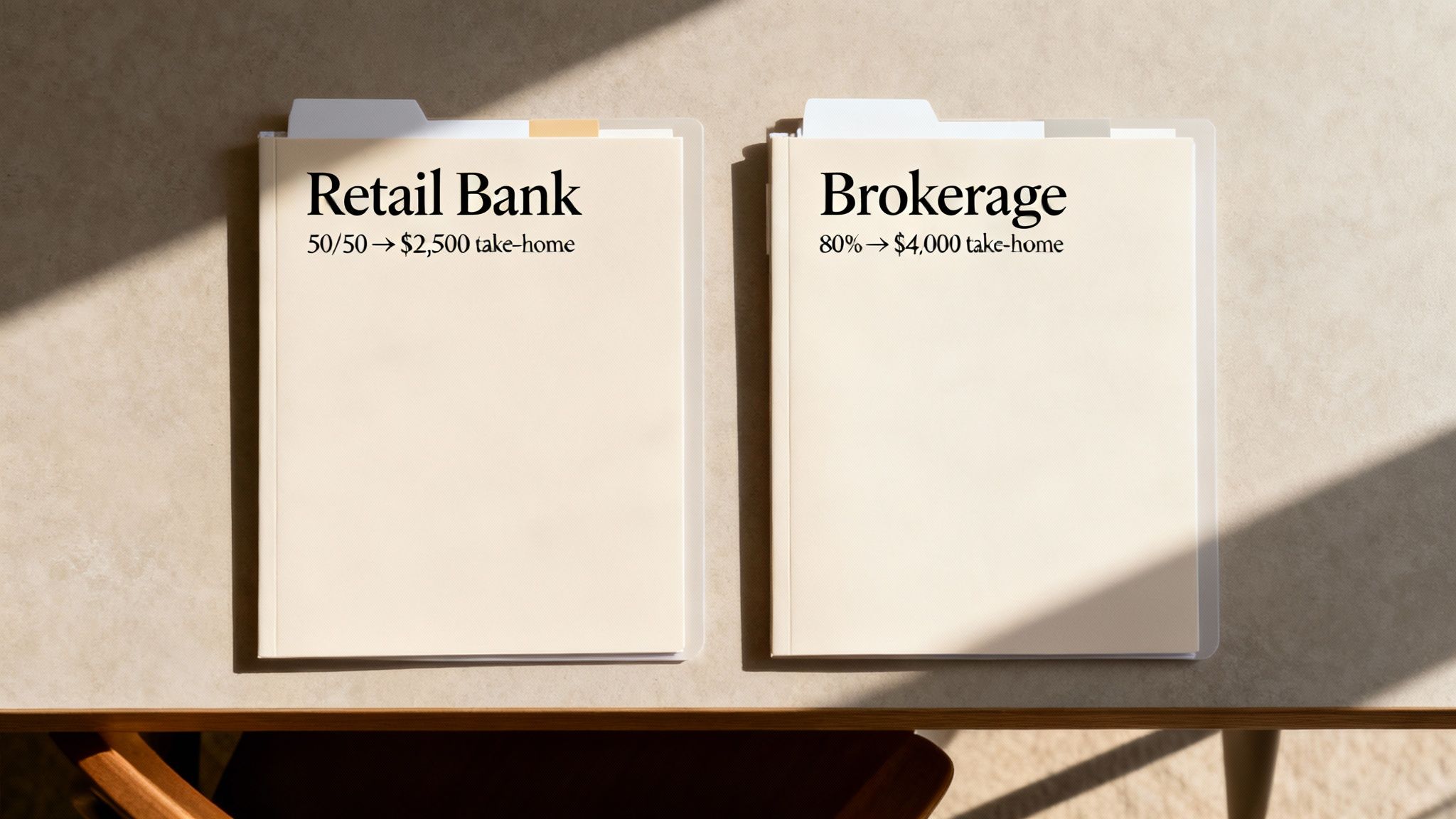

These two career paths offer a classic trade-off. A big retail bank often gives you more structure, support, and most importantly, a steady flow of leads from their marketing and branch network. But that support isn't free. Banks typically take a much larger piece of the pie, with splits often landing around a 50/50 split.

On the flip side, working for an independent mortgage brokerage is more of an eat-what-you-kill environment. You’re usually responsible for finding your own clients and building your own business. It requires more hustle and an entrepreneurial mindset, but the financial rewards can be enormous. Brokerages offer far better splits, where it’s common to keep 75%, 80%, or even more of the gross commission.

This table shows just how much the employer's model impacts your earnings on the same $5,000 gross commission.

| Factor | Independent Broker | Retail Bank |

|---|---|---|

| Gross Commission | $5,000 | $5,000 |

| Common Split | 80% to MLO | 50% to MLO |

| Your Take-Home | $4,000 | $2,500 |

| Difference | You earn $1,500 more | You earn $1,500 less |

That $1,500 difference is on one deal. Imagine closing just a few loans a month—the gap in annual income becomes massive. This is why driven MLOs who are great at building their own book of business gravitate toward the brokerage model.

The choice between a bank and a brokerage really boils down to your personality and goals. Do you value the safety net of a steady lead source, or are you motivated by the sky-high earning potential of being your own boss?

The good news is that the mortgage industry is always evolving to attract top producers. Forward-thinking firms, especially hybrid brokerages, are now offering splits that can push an MLO's total compensation past 1% of the loan amount. On a $500,000 loan, that means earning $5,000 or more, blowing past the old retail bank caps of 0.5-0.75%. This is a direct result of fierce competition for talent. If you can produce, lenders will pay up. You can discover more insights about these competitive commission structures.

Many companies also sweeten the deal with tiered commission structures. This means your split isn't set in stone for the year; it actually gets better as you close more loans.

You might start out with a 70% split, for example, but after hitting a certain volume target for the quarter, you automatically jump to 80% or even 90%. It’s a powerful model that directly rewards hard work and creates a clear path to increasing your income without having to switch employers.

Of course. Here is the rewritten section, crafted to sound like an experienced human expert and match the provided style examples.

Think of your commission rate and split as the foundation of your paycheck. But several other variables can add a few extra stories to the building. Not every loan is the same, and knowing the nuances is how you go from just closing deals to actually maximizing what you make on that $500,000 loan.

The type of loan you’re working on matters—a lot. For example, government-backed loans like FHA or VA loans often come with their own compensation rules or caps that you won't see on a standard conventional mortgage. On the flip side, jumbo loans (the big ones that go beyond what Fannie Mae and Freddie Mac will back) often have unique pricing and commission structures. They're more complex, sure, but they can also mean a bigger payday.

Here's where things get interesting. You'll often see origination fees and discount points on a loan estimate, and they can directly impact your wallet. An origination fee is what the lender charges to get the loan processed, and depending on your company's setup, a piece of that fee might flow directly into your commission.

Discount points are another key piece. These are simply fees a borrower pays upfront to buy down their interest rate. In many compensation plans, MLOs earn commission on those points, creating another way to add to your income from a single transaction. To really succeed, MLOs need to think beyond just the interest rate and focus on the entire deal structure by adopting robust contract management best practices that keep everything streamlined and buttoned up.

Your ability to navigate different loan products and fee structures directly impacts your bottom line. It’s not just about closing a deal; it's about closing the right deal for both your client and your paycheck.

Finally, let's talk about one of the biggest factors: you. A brand-new MLO just getting their feet wet will probably start on a standard commission plan with little room for negotiation. But that changes quickly.

A seasoned pro with a solid book of business and a reputation for closing loans can often negotiate much better terms. We're talking higher commission tiers, a more generous split, or access to more complex and higher-paying loan products that rookies don't get to touch.

As you build your career and prove your value, your leverage with any brokerage or bank grows. Your experience becomes a real financial asset, allowing you to command better compensation. This career path, colored in professionalism, is built to reward growth—the more skilled you become, the more you earn. It’s a field where your hard work and knowledge pay off directly.

Theory is great, but let's make these numbers real. To truly understand how much commission do loan officers make on a $500,000 loan, it helps to walk through a few day-in-the-life examples. These stories show just how much your experience and work environment can impact your paycheck.

We'll follow three different MLOs, each closing a single $500,000 loan.

Meet Alex. He's just starting his career at a big retail bank. He gets a steady stream of leads handed to him and the credibility of a well-known brand, which is a huge advantage. But his compensation reflects his entry-level status and the support system he has.

For a brand-new loan officer, this is a solid payday. The bank's structure gives him a chance to learn the business while earning a consistent income.

Now there's Maria. With a few years under her belt, she's built a solid network of realtors and past clients. She moved to an independent brokerage for more freedom and a better commission split. Her hustle and relationship skills really pay off here.

Maria earns more than double what Alex made on the exact same loan. This shows the massive financial upside of gaining experience and moving into a more entrepreneurial role.

Finally, we have David. He's a veteran MLO with a stellar reputation that brings clients to him. He commands a high commission rate and has negotiated a very aggressive split with his brokerage. His deep industry knowledge makes him an earning powerhouse.

David's take-home from a single deal is more than triple Alex's. That's the peak earning potential in this career. These scenarios paint a clear picture of financial growth over time, a topic you can explore further in our guide to the average mortgage loan officer salary.

These examples highlight a core truth of the mortgage industry: your income is a direct reflection of your effort and expertise. As you grow, so does your paycheck.

The path from Alex to David is paved with hard work and dedication. But the first step is getting your license, which is easier than ever with our fully online, NMLS-approved education and free exam prep.

Feeling inspired by the six-figure income potential? The path to becoming a licensed Mortgage Loan Originator is more straightforward than you might think, and our entire process is designed to get you there without the usual hassle. You don’t have to put your life on hold to chase this kind of career.

Our education is entirely online and fully approved by the NMLS Nationwide Multi State Licensing System and Registry, giving you the flexibility to prepare for this rewarding profession from anywhere. You can study from home, name your own hours, and build a career that fits your life—not the other way around.

We’re here to help you succeed from day one. That’s why our comprehensive exam prep package is included for free with your pre-licensing course. We believe in giving you everything you need to pass the SAFE MLO test with confidence, without any hidden fees or surprises.

Think of this education not as a hurdle, but as the simple first step toward unlocking the financial freedom detailed in this guide. The opportunity is right here, colored in potential and success.

The kind of money we've been talking about—like how much commission loan officers make on a $500,000 loan—is well within your reach. It all starts with getting the right education and passing your exam. We simplify that part so you can focus on what really matters: building your business and closing deals.

Getting licensed is the launchpad for a career where you can work from home, enjoy a real work/life balance, and directly control your income. Ready to take that first step? You can learn exactly how to become a Mortgage Loan Originator with our complete guide, which breaks down the entire process.

Even after breaking down the numbers, you probably still have a few questions floating around. It's a unique career path, and it makes sense to get the full picture before you jump in.

Let’s tackle some of the most common questions we hear from aspiring loan officers.

This really comes down to the business model of where you work. At big retail banks, it's pretty common for MLOs to get a modest base salary plus a commission on the loans they close. It’s a nice safety net to have, especially when you're just getting your feet wet.

On the other hand, many of the industry's top earners—especially those at independent mortgage brokerages—are on a 100% commission model. This is where the magic happens for those with an entrepreneurial drive. Your income is tied directly to your hustle, which means your earning potential is completely uncapped.

Faster than you'd think. Once you wrap up your NMLS-approved education and sail through the licensing exam, you can hit the ground running and start originating loans almost right away.

The typical mortgage takes about 30-45 days to close from the moment the application is submitted to the final funding. So, a motivated new MLO could realistically see their first commission check within two months of officially starting. It’s a field where you can ramp up to a serious income pretty quickly.

Yes and no. The commission percentage doesn't change, but your total earnings are directly tied to local real estate prices. This is a huge factor when you think about how much commission do loan officers make on a $500,000 loan.

Think about it like this: A standard $500,000 loan might be for a beautiful family home in a mid-sized city. That exact same house in a major metro area like Los Angeles or New York could easily be a $1,000,000 loan. An MLO in that market has the chance to earn double the commission for the same amount of work, which obviously makes a massive difference in their annual income.

Ready to launch a high-income career with the freedom to work from home? 24hourEDU makes getting your NMLS license straightforward with our fully online, NMLS-approved education and free exam prep. Start your journey to becoming a Mortgage Loan Originator today!

Unlock what is mortgage origination fee, how it’s calculated, and its impact on APR. Essential knowledge and negotiation tips for aspiring MLOs.

Deciding on a mortgage company vs bank? This guide breaks down the key differences in rates, loan options, and approval speed to help you choose wisely.

Wondering can i take the nmls exam online? Learn formats, prep tips, and deadlines to confidently tackle the NMLS exam online.

Learn how to get an nmls license in birmingham alabama: step-by-step guide and start your MLO career with streamlined online education.

Discover how to secure your mlo license arizona and enjoy a semi-retired lifestyle in Scottsdale with tailored online education and free exam prep.

Loan officers earn $2,500-$5,000 in gross commission on a $500,000 loan, typically 0.50%-1.00% in basis points. Learn how commission splits, employer type, and experience level impact your actual take-home pay as an MLO.

Your expert guide to the mortgage lender license texas. Learn about NMLS requirements, education, and the application process to start your career.

Does the Fed set mortgage rates? Get the definitive MLO guide that breaks down the Federal Reserve’s true impact on the mortgage market, inflation, and the 10-Year Treasury.

Learn how to obtain your mortgage lender license florida with a step-by-step checklist, timelines, and insider tips.

See why there are so many benefits to earning a mortgage lender license. Unlock higher earning potential, career flexibility, industry credibility, and diverse opportunities in the thriving mortgage industry.

Picture this: a thriving career with a high-income potential, set against the backdrop of one of Florida’s most unique and booming real estate markets. That’s exactly what’s waiting for you in The Villages. Becoming a mortgage loan officer here is your ticket into a commission-based career where you can work from home and name your own hours.

The Federal Reserve cut rates! Learn why this decision is great news for your MLO pipeline, boosting refinancing, increasing buyer confidence, and creating immediate marketing opportunities.