When you're looking at a mortgage application, one number stands out more than almost any other: the loan-to-value ratio, or LTV.

So, what is it? Simply put, LTV is a percentage that shows how much of a property's value you're borrowing. For instance, if a home is appraised at $400,000 and the buyer needs a $320,000 loan, their LTV is 80%. This straightforward calculation is one of the most critical risk assessment tools a lender has.

Understanding the Loan to Value Ratio

At its heart, the LTV ratio is all about risk. Think of a home's total value as a pie. The loan you're providing is one slice of that pie, and the borrower's down payment is the other. LTV tells you exactly how big the lender's slice is compared to the whole thing.

A smaller slice for the lender (a lower LTV) is always better because it means less risk. Why? Because the borrower has more "skin in the game" with their larger down payment, which creates a nice equity cushion right from the start. This simple concept is the foundation of almost every loan you'll ever work on.

The Role of LTV in Mortgages

As you start your journey as a Mortgage Loan Originator, you'll quickly see that LTV impacts nearly every aspect of a loan file. It’s far more than just a number on a form; it directly influences:

- Loan Approval: Lenders have firm LTV limits. If a borrower's ratio is too high, it can be an immediate deal-breaker.

- Interest Rates: A lower LTV often translates to a better interest rate. From the lender's perspective, a less risky loan deserves a better price.

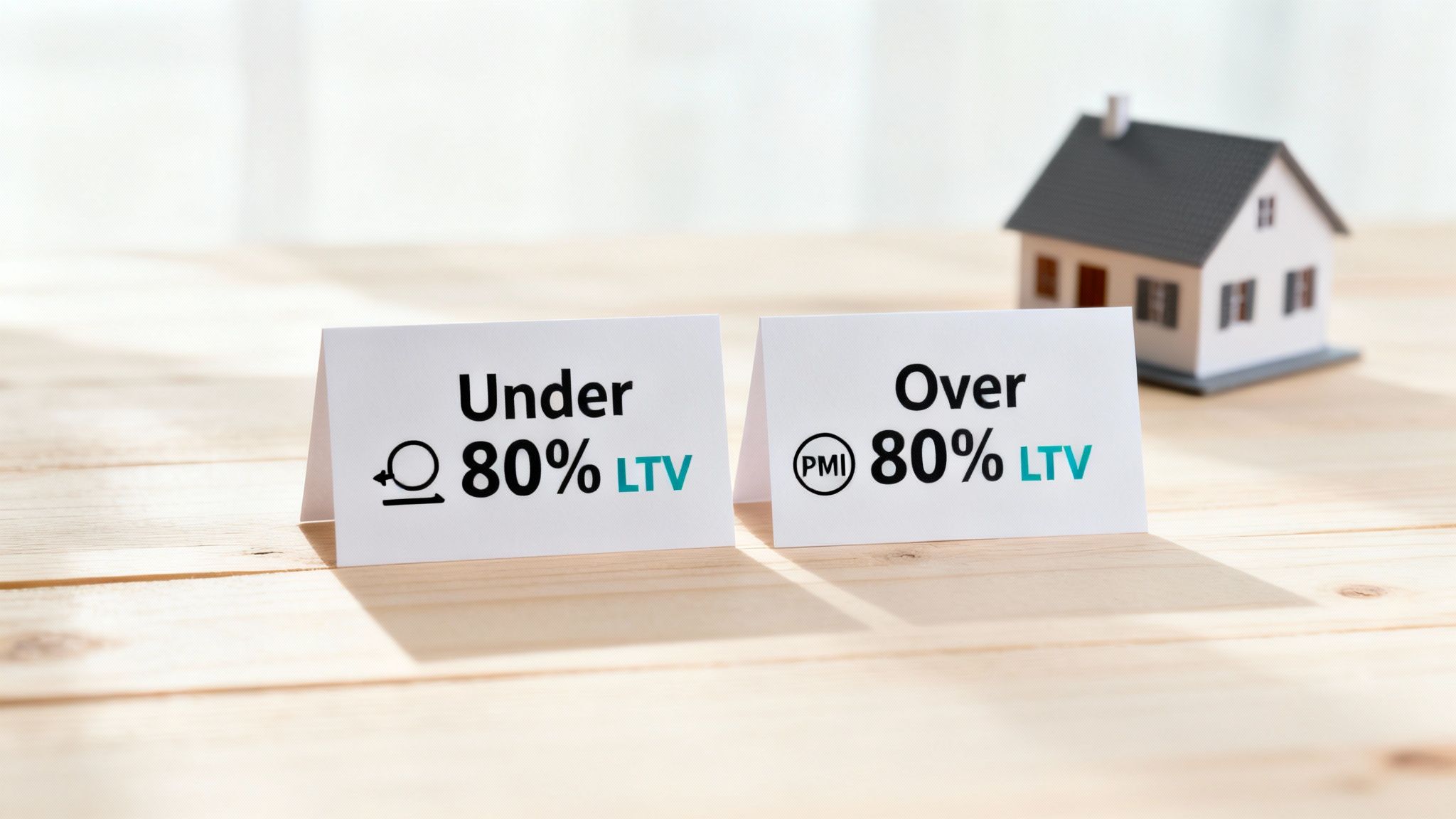

- Mortgage Insurance: This is a big one. For conventional loans, an LTV creeping above 80% almost always triggers the need for Private Mortgage Insurance (PMI).

The Loan to Value ratio isn't just about getting a loan approved; it's about the total cost of that loan over its lifetime. When you truly grasp this, you can give clients expert advice that saves them real money and builds the kind of trust that lasts a career.

Mastering this principle is a crucial first step on your path to becoming a successful MLO. With our fully online, NMLS-approved education—which includes our exam prep package for free—we make it easy to understand core concepts like this and launch your high-income career working from home. For example, LTV is especially important for products like a Home Equity Line of Credit (HELOC), where it determines eligibility and rates. You can learn more about What is a HELOC and how does it work.

How to Confidently Calculate LTV

As a Mortgage Loan Originator, calculating the LTV ratio will become second nature to you. It's a quick, essential step you'll perform in almost every client conversation. Thankfully, the formula is refreshingly simple and gives you an immediate snapshot of a loan's risk profile.

The core formula you'll use every single day is:

LTV = (Loan Amount / Property Value) x 100

This simple equation tells you exactly what percentage of the property's value is being financed. Now, here's a critical detail to lock in: lenders always use the lesser of the home's official appraised value or its purchase price for this calculation. This is a non-negotiable rule that protects the lender from over-lending if a buyer agrees to a price higher than what the market says the home is worth.

For a deeper dive into how appraisers fit into this process, you might find our guide on using the appraiser your mortgage broker recommends helpful.

Real-World LTV Calculation Examples

Let's walk through a few common scenarios you'll encounter with borrowers to see how this plays out in the real world.

Example 1: The Standard 80% LTV

This is the gold standard for many conventional loans. Hitting this number often means your borrower gets to avoid Private Mortgage Insurance (PMI), which is a huge selling point.

- Property Value: $400,000 (appraised value)

- Down Payment: $80,000 (which is 20% of the value)

- Loan Amount: $320,000

Calculation: ($320,000 / $400,000) x 100 = 80% LTV

Example 2: A High LTV for a First-Time Homebuyer

Many government-backed programs are designed to make homeownership more accessible, which means they allow for much higher LTVs.

- Purchase Price: $350,000

- Down Payment: $17,500 (a 5% down payment)

- Loan Amount: $332,500

Calculation: ($332,500 / $350,000) x 100 = 95% LTV

This higher LTV is extremely common, especially for first-time buyers, but it almost always means the borrower will have to pay for mortgage insurance.

Example 3: Cash-Out Refinance

In this situation, a current homeowner is tapping into their equity by taking out a new, larger loan.

- Appraised Value: $500,000

- Existing Mortgage Balance: $250,000

- New Loan Amount (including cash out): $375,000

Calculation: ($375,000 / $500,000) x 100 = 75% LTV

The Loan-to-Value (LTV) ratio is a cornerstone metric in the mortgage world, used globally to measure lending risk. A ratio below 80% is the magic number that signals lower risk to lenders and helps borrowers save money. Mastering these simple calculations will make you a more confident and capable MLO right from the start.

Why LTV Is a Lender's Most Trusted Metric

When a lender looks at a loan application, they’re really asking one simple question: “How risky is this deal?” The Loan-to-Value ratio gives them a direct, no-nonsense answer. It cuts through all the noise and tells them exactly how much of their own money is on the line if the borrower stops paying.

A high LTV is an immediate red flag. It means the borrower has very little of their own cash invested—what we call "skin in the game." To a lender, that small down payment looks like a thin safety net. Statistically, it also means the borrower is more likely to walk away if they hit a rough patch financially.

Gauging Borrower Commitment

Now, flip that around. A low LTV tells a completely different, and much happier, story. It shows the borrower is making a serious financial commitment right from the start, creating a hefty equity buffer. This buffer is the lender’s primary shield against loss.

If the market takes a dip or, worst-case scenario, the lender has to foreclose, that equity cushion makes it far more likely they can sell the property and get their money back. This is precisely why underwriters put so much weight on LTV when they’re making the big decisions.

The LTV ratio acts as a financial barometer for lenders. It not only predicts the likelihood of a borrower defaulting but also forecasts the potential financial loss if a default occurs. A lower LTV calms lender fears on both fronts.

Impact on Loan Terms and Approval

As an MLO, you need to drive home this point with your clients: LTV isn't just an internal metric for the bank. It directly hits their wallet and determines what kind of deal they can get.

-

Loan Approval: Forget about credit scores and income for a second. Many loan programs have hard LTV ceilings. If your client's LTV is too high, it’s an automatic "no," period.

-

Interest Rates: Lenders use better pricing to reward lower risk. A borrower with an 80% LTV is almost guaranteed to lock in a better interest rate than someone coming in with a 97% LTV. It’s that simple.

-

Mortgage Insurance: This is the big one. For most conventional loans, any LTV over 80% triggers the need for Private Mortgage Insurance (PMI). You have to make it clear to your borrowers that PMI protects the lender, not them, and it’s a direct cost added to their monthly payment.

The power of LTV goes way beyond just one loan. Deep-dive research has actually shown that the LTV ratio is a powerful predictor of housing market trends. Some studies even suggest it’s better than other common metrics at forecasting housing returns and rent growth, helping institutions make smarter portfolio decisions. If you're interested, you can explore the predictive ability of LTV in housing markets to see just how significant this metric is on a macro level. This is the kind of insight that separates the good MLOs from the great ones.

How LTV Directly Impacts Your Borrower's Loan

For your clients, the Loan-to-Value ratio isn't just another piece of industry jargon. It's one of the most critical numbers that will shape their monthly payment and the total cost of their home loan. As an MLO, your real value shines when you can translate a simple percentage into a clear financial reality for your borrowers. That's how you build trust that lasts a lifetime.

Think of LTV as a lender's risk gauge. A lower LTV tells them the borrower has significant "skin in the game," which almost always unlocks better terms. On the flip side, a high LTV means the lender is taking on more risk, and they'll adjust the loan terms to protect themselves—usually at the borrower's expense.

Unlocking Better Terms With a Lower LTV

In the world of conventional lending, 80% LTV is the magic number. When you can get a client to this point—either with a 20% down payment or through a refinance with plenty of equity—they're in the driver's seat.

This is the threshold where lenders roll out their most competitive interest rates. But the biggest win? It allows your borrower to completely sidestep Private Mortgage Insurance (PMI). That’s the costly monthly fee that protects the lender, not the homeowner. Guiding a client to that 80% LTV sweet spot can literally save them hundreds each month and thousands over the life of the loan.

The Real Cost of a Higher LTV

When a borrower’s LTV climbs above 80%, the financial picture gets a bit more complicated. To offset their increased risk, lenders will typically offer slightly higher interest rates and, more importantly, they'll require mortgage insurance.

This insurance isn't optional; it's a mandatory part of any high-LTV conventional loan. For clients who need to put less money down, you have to be crystal clear about this extra cost. For a deeper dive, our guide on what is mortgage insurance is a great resource to share so they understand the full financial picture.

How LTV Affects Loan Terms

To make it simple, the relationship between LTV and the kind of loan terms a borrower can expect is direct and predictable. The more equity they bring to the table, the better the deal gets.

| LTV Ratio | Lender Risk Level | Typical Interest Rate | PMI Requirement |

|---|---|---|---|

| 80% or Below | Low | Most Favorable | Not Required |

| 80.01% – 90% | Moderate | Standard | Required |

| 90.01% – 97% | High | Slightly Higher | Required |

As you can see, crossing that 80% line is what triggers the most significant changes, adding costs that impact a borrower's monthly budget.

Loan Programs and Their LTV Rules

The good news is that different loan programs were designed with different LTVs in mind, creating pathways to homeownership for almost everyone.

- Conventional Loans: The 80% LTV is the gold standard for avoiding PMI. Still, some programs push the limit as high as 97% LTV, letting buyers get in the door with just 3% down.

- FHA Loans: Backed by the government, these loans are perfect for buyers with smaller down payments, allowing an LTV of up to 96.5%.

- VA Loans: This is an incredible benefit for eligible veterans and service members. VA loans allow for up to 100% LTV, meaning zero down payment is required.

Knowing the rules for each of these programs is what makes you an invaluable guide. It's the core knowledge you'll use to match every client with the perfect mortgage for their unique situation and goals.

Actionable Strategies for a Lower LTV

Understanding the loan-to-value ratio is step one. Step two is using that knowledge to help your clients win. As an MLO, your guidance can directly lead borrowers to a lower LTV, potentially saving them thousands over the life of their loan.

Think of these strategies as the tools in your belt. Using them helps you build client trust and structure better, more affordable loans that get to the closing table.

Increase the Down Payment

The most straightforward way to lower LTV is to put more money down. A larger initial investment from your client reduces the amount they need to finance, which instantly improves their LTV ratio and makes their application look much stronger to underwriters.

But "personal savings" isn't the only answer. It's crucial to explore every available avenue with your clients, as many borrowers have no idea they have options beyond what’s sitting in their checking account.

- Gift Funds: Many loan programs are perfectly fine with borrowers using money gifted from close relatives. Proper documentation is the key here, but it's a powerful way to significantly boost a down payment.

- Down Payment Assistance (DPA) Programs: Countless state and local programs offer grants or low-interest loans specifically to help homebuyers cover their down payment and closing costs.

- Retirement Account Loans: Some borrowers might be able to take a loan against their 401(k). This route requires careful consideration of the long-term impacts, but for the right client, it can be a game-changer.

Negotiate a Lower Purchase Price

Here’s a powerful but often overlooked tactic: negotiate a lower sale price on the home. Because the LTV is calculated using the lesser of the purchase price or appraised value, getting the seller to come down on the price directly shrinks the final ratio.

For instance, say a home appraises for $400,000, but your buyer successfully negotiates the price down to $390,000. Their $40,000 down payment now creates a much healthier LTV than it would have at the higher price. This strategy is especially potent in a buyer's market or when a property has been sitting for a while.

Strategies for Refinancing Homeowners

For your clients looking to refinance, the path to a lower LTV is all about leveraging the equity they’ve already built up. Time and smart decisions can dramatically improve their financial standing.

A lower LTV during a refinance isn't just about snagging a better rate; it's about unlocking the home's built-up value. This can mean wiping out PMI, pulling cash out for other goals, or simply enjoying a lower monthly payment.

Property appreciation is a homeowner's best friend. If the local market has been hot since the original purchase, a new appraisal could reveal a much lower LTV without the owner having to do a thing.

On top of that, strategic home improvements that boost the property's appraised value can be another highly effective way to push the LTV down.

For real estate investors, these principles are mission-critical. For those using specific models like the BRRRR strategy real estate, hitting a target LTV after a renovation is absolutely essential for a successful cash-out refinance to fund the next deal. By guiding them through these steps, you help them grow their portfolio and secure a stronger financial future.

Reading the Market Through LTV Trends

Understanding what loan-to-value means for a single borrower is essential, but seeing it on a macro level is what separates good Mortgage Loan Originators from truly great ones. When you start tracking average LTV trends across the market, you gain a powerful lens into the health of the housing sector and the current mood among lenders.

It’s almost like being able to read the industry’s collective mind.

When you see average LTVs start to climb, it’s a clear signal that the economic winds are shifting. This almost always points to growing lender confidence. They’re willing to loosen their underwriting standards a bit and take on more risk because they feel good about where property values and the overall economy are headed.

On the flip side, when average LTVs begin to fall, it suggests a more cautious, risk-averse mindset. Lenders are likely tightening their belts in response to economic jitters, forcing borrowers to bring more of their own skin to the game. This insight is gold when you're managing client expectations in a tough lending environment.

What the Data Reveals

This isn't just theory; it's a data-driven strategy. Looking at the numbers, LTV ratios can swing pretty significantly over time and from one region to another. For example, in the second quarter of 2025, the 75th percentile of the original LTV ratio in the U.S. was 83%.

This tells us that a full quarter of all new loans were written with an LTV of 83% or higher—a noticeable jump from previous quarters where the median LTV was closer to 75%. You can explore more on LTV trends via FRED Economic Data to see these shifts for yourself.

Having a solid grasp on these high-level LTV movements allows you to have smarter, more informed conversations with your clients. You can explain why rates are where they are or why underwriting suddenly feels tighter, positioning yourself not just as an originator, but as a genuine market expert.

This knowledge empowers you to set realistic expectations from the get-go and navigate any market conditions with confidence. As an MLO, your ability to interpret these trends and communicate them clearly is a skill that will absolutely set you apart and help you build lasting client trust.

Common Questions About Loan to Value

As you get ready to become a Mortgage Loan Originator, you'll quickly realize that clients (and even other pros) ask the same few questions about the loan-to-value ratio over and over.

Having clear, confident answers on hand is a great way to build trust and show you know your stuff.

What Is a Good LTV Ratio for a Mortgage?

The magic number here is 80%. An LTV of 80% or lower is the gold standard in the mortgage world.

When a borrower hits this mark, lenders see the loan as a much lower risk. The biggest perk? It usually means the borrower gets to skip paying for Private Mortgage Insurance (PMI). Getting under that 80% threshold is also the ticket to unlocking the best, most competitive interest rates a lender has to offer.

Can You Get a Mortgage with a High LTV Ratio?

Absolutely. In fact, that’s exactly what government-backed loan programs were created for.

FHA loans, for instance, allow for an LTV all the way up to 96.5%. For qualified veterans, VA loans can go even higher—up to a full 100% LTV. These programs are fantastic for making homeownership happen with little to no down payment, but they almost always come with some form of mortgage insurance to offset the lender's risk.

How Does Refinancing Affect LTV?

When you refinance, your LTV gets a complete do-over. It's recalculated using your current outstanding loan balance against a brand-new appraisal of your home's value.

If your home's value has gone up since you first bought it, your new LTV will be lower. This is great news! It could land you a better interest rate or be just what you need to finally cancel your PMI payments. On the flip side, a cash-out refinance adds to your loan amount, which will push your LTV higher.

LTV only looks at the main mortgage versus the home's value. But there's another term you'll see: Combined Loan to Value (CLTV). This includes all liens on the property, like a primary mortgage plus a home equity line of credit (HELOC). Lenders look at CLTV to get the full picture of debt risk when considering a second mortgage.

Another crucial metric you'll need to master is the debt-to-income ratio, which you can learn about in our guide on how to calculate debt to income ratio.

Ready to turn this knowledge into a high-income career where you can work from home and name your own hours? 24hourEDU makes it easy to get your Mortgage Loan Originator license with our fully online education, which is approved by the Nationwide Multi-State Licensing System & Registry (NMLS). Our courses are designed for your success and include our exam prep package for free. Start your journey today at https://24houredu.com.

5 Comments