When you see a mortgage origination fee on your loan documents, what does it actually mean? Think of it as the lender’s charge for getting your entire loan application processed, packaged, and ready to go. It’s a standard closing cost that covers all the administrative legwork, from verifying your income to underwriting the loan and preparing the final paperwork.

This fee is almost always calculated as a percentage of your total loan amount. It’s not just a random number; it represents the essential services that make your home loan happen.

What Your Origination Fee Actually Covers

The easiest way to understand the origination fee is to think of it like a setup charge for a new utility service. Once a lender agrees to fund your home loan, a whole lot of work kicks off behind the scenes. This fee is how the lender gets compensated for the time, people, and resources needed to get your mortgage from application to the closing table.

It’s one of the most common closing costs you’ll see, and for anyone aspiring to become a Mortgage Loan Originator (MLO), understanding it is absolutely fundamental. This isn’t just another line item—it’s the cost of the engine that drives the whole loan process forward.

So, what exactly are you paying for when you see this charge? The origination fee bundles several critical tasks into a single, upfront cost. Without these services, a loan simply can’t get off the ground.

To give you a clearer picture, here’s a breakdown of the key administrative tasks that your mortgage origination fee typically funds. This table shows you exactly what value you’re getting for that fee.

What Your Origination Fee Actually Covers

| Service Component | What It Means for Your Loan |

|---|---|

| Loan Processing | This is the heavy lifting of gathering and organizing all your financial documents—pay stubs, tax returns, bank statements, you name it. |

| Underwriting | The underwriter conducts a deep-dive risk assessment, verifying your financial health to officially approve (or deny) the loan. |

| Document Preparation | This covers the creation of all the complex legal paperwork required for closing, ensuring every single detail is accurate and compliant. |

As you can see, these aren’t minor tasks. They require a team of specialists, from processors to underwriters, and the origination fee helps cover their expertise and time. It’s a direct payment for the labor required to structure your financing correctly.

Ultimately, this fee ensures every detail is handled properly, paving the way for a smooth and successful closing. For an MLO, being able to clearly explain this value to a client is crucial for building trust. It turns what looks like just another fee into a tangible, necessary service.

How Lenders Calculate Your Origination Fee

When you pull back the curtain on what is a mortgage origination fee, the math itself is surprisingly simple. Lenders almost always calculate this fee as a percentage of the total loan amount, not some arbitrary flat number. This makes sense—it allows the fee to scale with the size and complexity of the loan they’re working on.

Typically, you’ll see origination fees land somewhere between 0.5% and 1% of the loan principal. While that might not sound like a lot, it adds up to a significant cost that borrowers need to be ready for at the closing table.

For any aspiring Mortgage Loan Originator, being able to walk a client through this calculation is a must-have skill. It demystifies a major closing cost and starts building that all-important foundation of trust from day one.

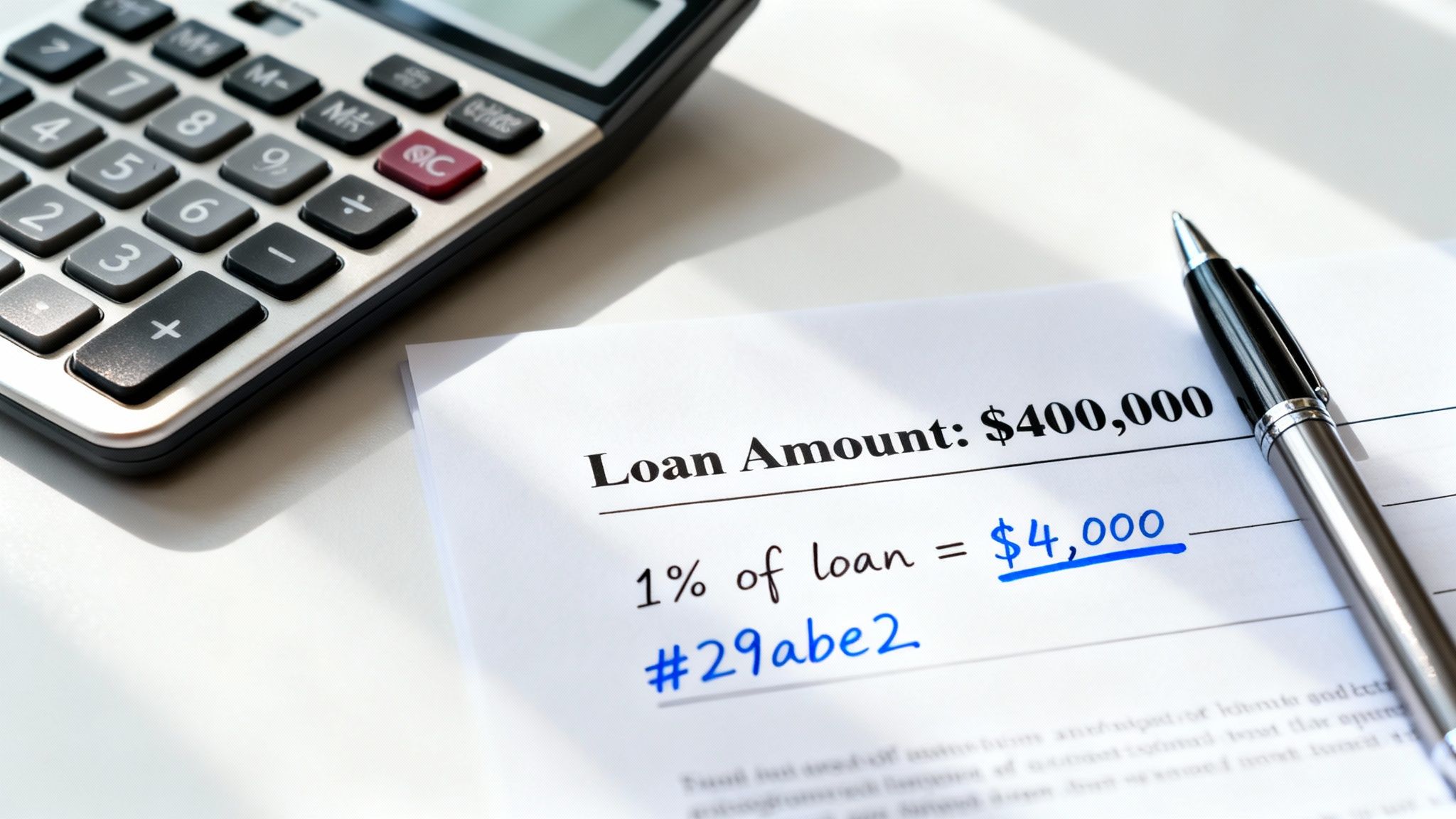

Breaking Down the Math with an Example

Let’s look at a real-world scenario to see exactly how this works. Imagine a homebuyer is getting a mortgage for $400,000. If their lender charges a pretty standard 1% origination fee, the calculation is straightforward.

Loan Amount:

$400,000Origination Fee Percentage:

1%(or 0.01)Calculation:

$400,000 x 0.01 = $4,000

In this case, the borrower pays a $4,000 origination fee. This fee is direct compensation for all the lender’s behind-the-scenes work to get the loan approved and funded.

The operational expense for lenders to originate a mortgage is no small thing, hitting around $11,800 in Q2 2025. Even though that number is an improvement, it shows why these fees are a standard part of doing business. You can review the latest data on mortgage origination costs to get a better handle on these lender expenses.

Key Factors Influencing the Percentage

Not all origination fees are identical. The exact percentage a lender quotes can shift based on a few key things about the borrower and the loan itself.

A strong credit score and a clean, straightforward loan application can often lead to more favorable terms, including a lower origination fee. Lenders see these borrowers as lower risk, and that can translate directly into savings.

Here are a few factors that can move the needle on that percentage:

Credit Score: A borrower with a high credit score is less of a risk. To compete for their business, lenders will often offer a lower origination fee, sometimes closer to that 0.5% mark.

Loan Complexity: A loan for a self-employed person with variable income is going to require a lot more underwriting work than a simple W-2 employee’s application. That extra effort can lead to a higher fee.

Lender Policies: At the end of the day, every bank and mortgage company has its own fee structure. This is why shopping around with a few different lenders is so important—you can find significant differences in fees for the very same loan.

Finding the Origination Fee on Loan Documents

Wading through mortgage paperwork can feel overwhelming, but thankfully, federal regulations have made it much easier to pinpoint your costs. When you need to find the mortgage origination fee, you really only need to look at two key documents: the Loan Estimate and the Closing Disclosure.

These forms aren’t just random stacks of paper; they’re standardized to be crystal clear, making sure you know exactly what you’re paying. For any aspiring Mortgage Loan Originator, mastering these documents is a foundational skill. Guiding a client through them confidently is one of the fastest ways to build trust and prove your expertise.

The Consumer Financial Protection Bureau (CFPB) created these forms to bring much-needed transparency to the lending process and get rid of those nasty surprises at the closing table. This standardization is a massive win for both borrowers and the MLOs who serve them.

Locating the Fee on Your Loan Estimate

The first time you’ll see the origination fee is on the Loan Estimate. Your lender must give you this document within three business days of receiving your loan application. Think of it as a detailed preview of the estimated costs of your mortgage.

Ready to find the fee? Just flip to Page 2 and look under the “Loan Costs” section.

Section A Origination Charges: This is ground zero. It’s where the lender’s main fees are laid out in plain sight.

Line Item 1: The fee is almost always listed right here, typically shown as both a percentage of the loan and the actual dollar amount.

Keep in mind, this figure is the lender’s best guess at this early stage. It’s a crucial number to look at, especially when you’re comparing offers from different lenders.

Comparing with the Closing Disclosure

The Closing Disclosure is the final, official breakdown of your loan terms and costs. You’ll get this document at least three business days before you’re scheduled to close, giving you time to review everything. It locks in all the final numbers, including the precise mortgage origination fee.

Just like on the Loan Estimate, you’ll find the final origination fee on Page 2 in Section A Origination Charges. The layout is nearly identical, making it simple to compare the two.

By law, the origination charge listed in Section A of your final Closing Disclosure cannot be higher than what was quoted on your initial Loan Estimate, unless there’s a valid “changed circumstance.” This is a huge protection for borrowers.

This rule gives you certainty and stops lenders from hiking up their main fee at the last minute. For an MLO, understanding this regulation is key. It helps you explain to clients why some third-party costs might shift slightly, but this specific fee is locked in.

For a complete rundown of all the paperwork involved in the loan process, our mortgage documentation checklist is an invaluable resource for anyone on the path to becoming an MLO.

How Origination Fees Drive Up Your APR

This is a spot where a lot of borrowers get tripped up, and it’s exactly where a great MLO can provide serious value. One of the biggest myths in lending is that a loan’s interest rate and its APR are the same thing. They absolutely are not, and the origination fee is one of the main reasons why.

The Annual Percentage Rate (APR) gives you the true cost of borrowing money. Think of it as the all-in price tag because it bundles the interest rate together with other lender costs—most importantly, the mortgage origination fee.

Breaking Down APR vs. Interest Rate

Here’s a simple way to think about it: the interest rate is like the sticker price of the loan, but the APR is the “out-the-door” price. It shows you what you’re really paying each year as a percentage, which is critical for making an apples-to-apples comparison between different loan offers.

For MLOs who really want to nail this down for their clients, it helps to understand the mechanics behind the numbers. A great way to sharpen these skills is to master the PMT function in Excel for accurate loan payment calculations.

Seeing the Trade-Off in Action

A loan with a lower advertised interest rate might look like a no-brainer, but a hefty origination fee can flip the script entirely. When that fee gets rolled into the loan, it bumps up the total amount you’re financing, which in turn pushes the APR higher.

Let’s look at a real-world comparison for a $300,000 loan:

| Lender A | Lender B | |

|---|---|---|

| Interest Rate | 6.50% | 6.75% |

| Origination Fee | 1.5% ($4,500) | 0.5% ($1,500) |

| APR | 6.68% | 6.81% |

At first glance, Lender A’s lower interest rate seems more attractive. But look closer. Its higher origination fee means its APR is actually higher, making it the more expensive loan over time.

The APR is the single most powerful tool for comparing loan offers fairly. A sharp MLO always steers the conversation toward the APR—not just the flashy interest rate—to help their client make the smartest financial move.

Getting this right is a fundamental skill for any successful Mortgage Loan Originator. It’s how you turn confusing financial jargon into clear, straightforward advice that can save your clients thousands and build the kind of trust that lasts a career.

Negotiating Origination Fees Like a Pro

Here’s something a lot of borrowers don’t realize: the origination fee isn’t always set in stone. While it’s a standard charge on almost every mortgage, it’s often negotiable. With the right approach, you can shave hundreds or even thousands off this closing cost. For future MLOs, understanding this flexibility is a huge part of delivering real value to your clients.

Success here really boils down to two things: preparation and leverage. A smart borrower—or an MLO guiding them—can build a strong case for better terms. It’s all about showing the lender you’re a well-informed and desirable client they don’t want to lose.

Create Leverage by Shopping Around

The single most powerful tactic is to get Loan Estimates from several different lenders. It’s that simple. Once you have competing offers in hand, you’ve instantly created leverage. You can then circle back to your preferred lender and ask, “Can you match or beat this competitor’s lower origination fee?”

This strategy works because the mortgage industry is fiercely competitive. Lenders are fighting for your business, and many are willing to trim their profit margin to lock in a high-quality loan. When comparing these offers, it’s crucial to understand the full picture, including the differences between a mortgage broker vs a bank lender, as their fee structures can look quite different.

Your Credit Score Is a Bargaining Chip

In any loan negotiation, a strong credit profile is your best friend. Lenders see borrowers with high credit scores and low debt-to-income ratios as low-risk. To attract and keep these prime customers, they are often much more willing to offer favorable terms, including a reduced origination fee.

Don’t ever be afraid to just ask. A simple, polite question like, “I have a strong credit history and another offer with a lower fee. Is there any flexibility on your origination charge?” can open the door to significant savings.

Understanding the Lender’s Position

It also helps to see things from the lender’s perspective. In Q2 2025, mortgage lenders earned an average profit of $950 for every loan they originated, a nice improvement from the year before. This data, available from the MBA’s look at lender profitability, shows they have some room to maneuver on certain fees to win over a great applicant.

Ultimately, negotiation is about showing the lender your value. By shopping around, highlighting your solid financial standing, and asking directly, you can often knock down this key closing cost and make your home loan that much more affordable.

Why This Knowledge Builds Your MLO Career

Getting a handle on the mortgage origination fee isn’t just about checking a box to pass the NMLS exam. It’s about laying the groundwork for a career built on trust with your clients. A deep, practical understanding of these costs is what separates a basic loan processor from a genuine financial advisor—and in a crowded market, that distinction is everything.

When you can break down complex fees with confidence, you’re not just selling a loan; you’re empowering your clients to make smarter financial choices. That ability is the secret sauce to earning referrals and building a high-income career with the flexibility you’ve always wanted. For MLOs who want to go even deeper, understanding advanced metrics like debt yield provides an even clearer picture of how lenders see financial risk.

Becoming a Trusted Advisor

In this industry, your expertise is your most valuable asset. The market is always moving, and knowledgeable professionals are in high demand. In fact, mortgage originations saw a significant comeback in Q3 2025, with $512 billion in new mortgages funded. This surge in activity, detailed in this New York Fed report, underscores the growing need for MLOs who can expertly guide homebuyers.

The most successful MLOs don’t just sell loans—they build relationships. When you master topics like origination fees, you show clients you’re committed to their best interests. That’s how a one-time transaction turns into a long-term professional connection.

This client-first mindset is at the very core of what it means to be a modern MLO. To learn more about the role and its responsibilities, check out our guide on what is an MLO.

Our fully online, NMLS-approved education makes getting your license incredibly easy. We’ve designed our program to get you licensed efficiently, and we even include our comprehensive exam prep package for free. We give you the tools you need to launch a rewarding career as a Mortgage Loan Originator with total confidence.

Your Top Questions About Origination Fees, Answered

As a Mortgage Loan Originator, you’re the expert your clients turn to for clarity. Understanding the common questions around origination fees is key to building that essential trust. Let’s break down what borrowers are most likely to ask.

Are Origination Fees Unavoidable?

While extremely common, origination fees aren’t set in stone for every single loan. You’ll often see lenders advertising “no-origination-fee” loans as a way to stand out and attract borrowers. It sounds like a slam-dunk deal, but there’s always a catch.

Lenders have to cover their costs somehow. Typically, they’ll make up for that missing fee by charging a slightly higher interest rate over the life of the loan. A sharp MLO knows how to run the numbers and show a client the total cost comparison—helping them see which option is really the better deal in the long run.

Can I Just Roll the Origination Fee into My Loan?

Absolutely. In most situations, borrowers can finance the origination fee by adding it to their total loan balance. This is a popular move for anyone trying to reduce the amount of cash they need to bring to the closing table.

It’s a great option for cash flow, but you have to explain the long-term impact. When you finance the fee, you’re also paying interest on it—for decades. That $4,000 fee could end up costing your client a whole lot more by the time the loan is paid off.

What’s the Difference Between Origination Fees and Discount Points?

This is a big one and a common point of confusion for borrowers. Both are paid at closing, but they do completely different jobs. Making this distinction crystal clear is a huge value-add for your clients.

Mortgage Origination Fee: Think of this as the lender’s fee for service. It covers the administrative work of processing the application, underwriting the file, and getting the loan ready. It pays for the work that’s already been done.

Discount Points: This is optional, prepaid interest. A borrower chooses to pay points upfront to buy down their interest rate, which lowers their monthly payment for the entire loan term.

Here’s a simple way to frame it: the origination fee is for the lender’s work, while discount points are an investment in a lower rate.

Ready to become the expert who can answer these questions with total confidence? At 24hourEDU, we make getting your MLO license easy with our online, NMLS-approved education. Our course even includes our exam prep package for free, giving you everything you need to launch your high-income career. Enroll today at https://24houredu.com.