The biggest difference really boils down to how you get the money and how you pay it back. A home equity loan gives you a single, lump-sum payment with a fixed interest rate, which is perfect for big, one-time projects. A HELOC (Home Equity Line of Credit), on the other hand, works more like a credit card that's secured by your home. It gives you a revolving line of credit with a variable rate, making it a great fit for ongoing or unpredictable costs.

Decoding Home Equity Loan vs. HELOC

Once you've built up equity in your home, you're sitting on a valuable financial asset. Tapping into it can be a smart move for funding major life events, consolidating high-interest debt, or just having a safety net for unexpected expenses. The two main ways to do this are with a home equity loan or a HELOC, but they couldn't be more different in how they work.

Getting a handle on their core mechanics is the first step to making the right call for your own financial situation. This isn't just about getting cash—it's about choosing the right structure, payment plan, and interest rate that actually matches your goals.

The Core Structural Differences

Think of a home equity loan as a "second mortgage." You get the entire loan amount at once, right after closing. From there, you start paying it back in fixed monthly installments over a set period, like 10 or 15 years. The predictability is the main draw here; your payment will never change.

A HELOC offers a completely different kind of flexibility. Instead of one big payout, you get a line of credit that you can draw from whenever you need it during a specific "draw period," which usually lasts up to 10 years. During this time, you can borrow funds, pay them back, and borrow again, much like you would with a credit card.

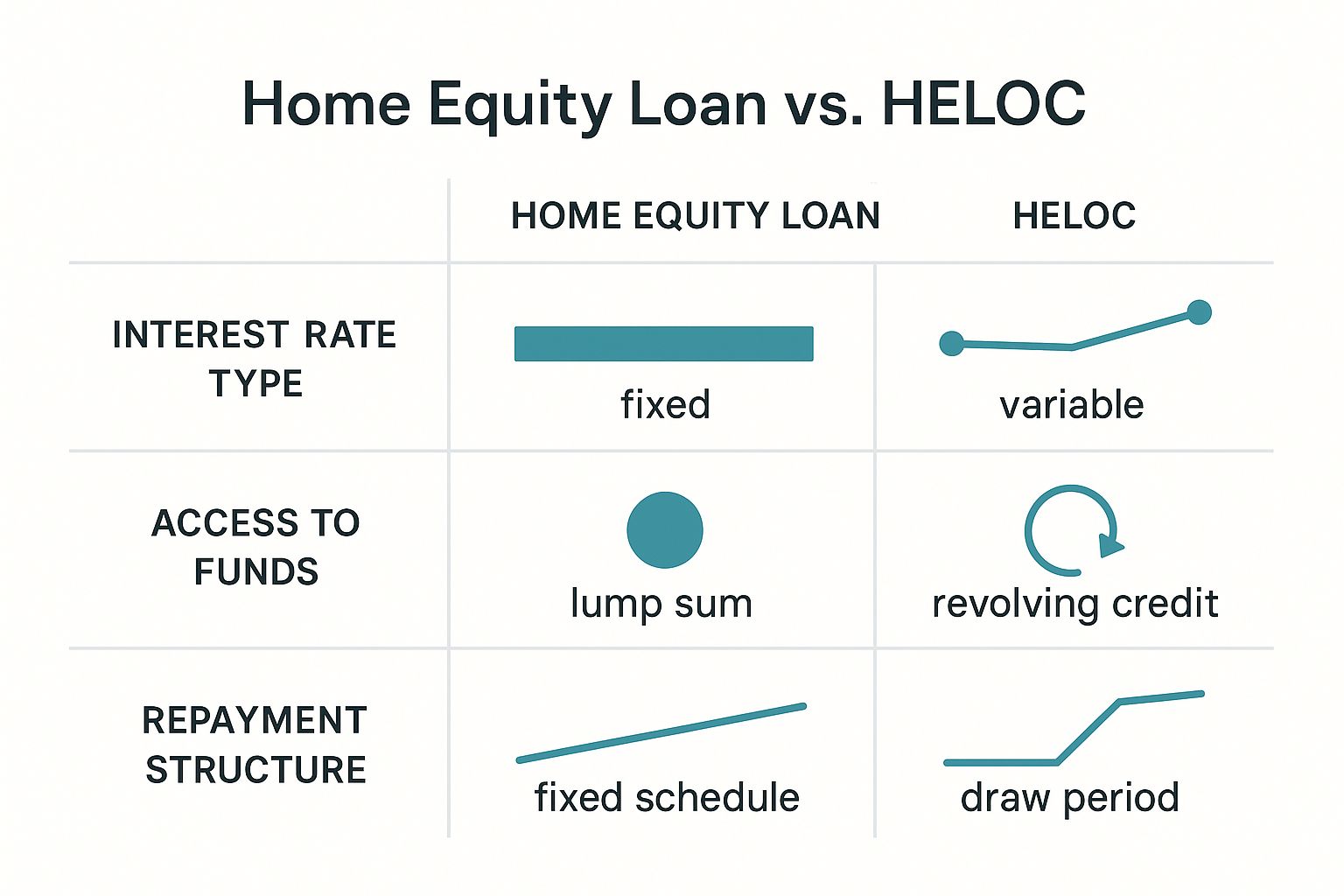

This visual breaks down how each product works when it comes to accessing funds, interest rates, and repayment.

As the chart shows, your choice really depends on what you value more: the stability of a fixed-rate, one-time loan or the adaptability of a variable-rate credit line you can use on your own terms.

Lump Sum vs. Revolving Credit

Home equity loans and HELOCs are structured in fundamentally different ways, which directly impacts how you can use them. A home equity loan is a closed-end loan that gives you a lump sum upfront, usually up to 80% of your home's equity. You'll have fixed monthly payments for a set term, so you always know what to expect.

In contrast, a HELOC is an open-ended, revolving line of credit. It allows you to draw funds as you need them during the draw period, but the interest rates are typically variable and can change with the market. If you want to see how these options stack up against others, you can discover more insights about borrowing options on kemba.org.

The decision really hinges on one question: Do you need a predictable, one-time amount for a specific project, or do you need flexible access to cash for ongoing or uncertain expenses?

For a quick overview, this table puts the most important features side-by-side.

Home Equity Loan vs. HELOC At a Glance

| Feature | Home Equity Loan | HELOC (Home Equity Line of Credit) |

|---|---|---|

| Loan Structure | A one-time lump-sum payment received upfront. | A revolving line of credit you can draw from as needed. |

| Interest Rate | Typically a fixed interest rate for the life of the loan. | Almost always a variable interest rate that can change over time. |

| Monthly Payments | Predictable, fixed monthly payments of principal and interest. | Payments can fluctuate based on the amount you've borrowed and interest rate changes. |

| Best For | Large, one-time expenses like debt consolidation or a major renovation. | Ongoing projects, emergency funds, or expenses with unknown final costs. |

| Flexibility | Less flexible; funds are disbursed once, and repayment begins immediately. | Highly flexible; borrow, repay, and borrow again during the draw period. |

How Interest Rates and Payments Really Work

When you dig into the mechanics of a home equity loan versus a HELOC, you find they’re fundamentally different animals. How they handle interest and structure your payments is what really sets them apart, and this choice will have a direct impact on your budget for years to come.

The core of it comes down to one thing: do you value predictable, stable payments, or do you need more flexibility, even if it comes with some uncertainty?

The Predictability of a Home Equity Loan

Think of a home equity loan as the financial equivalent of a straight, predictable road. It comes with a fixed interest rate, meaning the rate you get on day one is the rate you'll have for the entire life of the loan.

This setup creates a completely predictable monthly payment. You’ll know exactly what you owe every single month, which makes long-term budgeting a breeze. There are no surprises, no matter how much the economy zig-zags.

For example, say you borrow $50,000 to finally gut that old kitchen. With a home equity loan, your repayment schedule is locked in from the start. That kind of certainty is a huge relief when you’re managing a big, one-time project.

The Two Phases of a HELOC

A HELOC, on the other hand, operates on a completely different framework. It’s built for flexibility, using a variable interest rate and operating in two distinct stages.

Your interest rate isn't locked in. Instead, it’s tied to a benchmark index—almost always the U.S. Prime Rate. When the Federal Reserve adjusts rates and the Prime Rate moves, your HELOC rate moves right along with it. This means your monthly payment can change, making it a bit trickier to budget for.

To really understand it, you have to look at its two distinct phases.

The critical trade-off is clear: a home equity loan offers the security of a fixed payment, while a HELOC provides the flexibility of a credit line at the cost of potential rate changes.

1. The Draw Period

This is the first phase, and it’s when the HELOC acts like a credit card. It typically lasts for up to 10 years, and during this window, you can draw funds as you need them, up to your credit limit.

- Payment Structure: Your required payments are often interest-only. You’re just covering the interest on the money you’ve actually borrowed, not paying down the principal.

- Flexibility: This is the magic of a HELOC. You can borrow, pay it back, and borrow again. It’s a revolving line of credit perfect for ongoing projects or as a financial safety net.

- Example: Let's say you have a $75,000 HELOC but only use $20,000 for a bathroom remodel. Your minimum payment is calculated only on the interest for that $20,000, keeping your initial costs low.

2. The Repayment Period

When the draw period ends, the borrowing stops. You’ve now entered the repayment period, which can last anywhere from 10 to 20 years.

- Payment Structure: Your outstanding balance is converted into a traditional loan. From this point on, your monthly payments will include both principal and interest, chipping away at the total amount you owe.

- Payment Shock: This is a crucial point to prepare for. If you were only making small, interest-only payments, the switch to principal-and-interest payments can feel abrupt and significantly increase your monthly bill. It’s a phenomenon known as "payment shock."

- Continued Variability: Don’t forget, the rate is usually still variable during this phase. If the Prime Rate goes up, your now-larger payments could climb even higher.

A Deeper Look at the Pros and Cons

When you're trying to decide between a home equity loan and a HELOC, you’re really weighing stability against flexibility. It's not just about running the numbers; it’s about figuring out which one fits your personality, your project, and your stomach for risk.

Let's move past the textbook definitions and get into what these choices actually feel like in the real world. The best option really hinges on how you plan to use the money and how comfortable you are with a little bit of economic uncertainty. Think of a home equity loan as a fortress of predictability, while a HELOC is more like an open road of possibility.

The Home Equity Loan: Stability and Structure

The biggest draw of a home equity loan is its rock-solid predictability. The second you sign the paperwork, you know exactly what your monthly payment will be for the life of the loan. For anyone who dislikes financial surprises, this certainty is a huge relief.

- Pro: Predictable Payments: With a fixed interest rate, your payment is the same every single month. This makes budgeting a breeze because there are no surprises down the line.

- Pro: Fixed-Rate Security: If you think interest rates are on the rise, locking in a fixed rate now can save you a ton of money over the long haul.

But that stability has a trade-off: you get the entire loan amount in one check, and you start paying interest on all of it right away. It doesn't matter if the money is sitting in your bank account untouched—the interest clock is already ticking.

The core decision in the "home equity loan vs HELOC" debate often boils down to a choice between the psychological comfort of a fixed payment and the financial risk of a variable one.

The HELOC: Flexibility and Financial Freedom

A Home Equity Line of Credit, on the other hand, is all about flexibility. It’s less like a loan and more like a financial tool you keep in your back pocket for when you need it. This makes it a perfect match for projects where costs are unknown or will pop up over several months or years.

- Pro: Borrow As You Go: You only pull out money when you need it, and you only pay interest on the amount you’ve actually used. If you don't need all the cash at once, this can be a much cheaper way to borrow.

- Pro: Reusable Credit: During the "draw period," a HELOC works just like a credit card. You can borrow money, pay it back, and borrow it again without having to fill out another application.

The catch? That flexibility comes with a variable interest rate. HELOC rates are usually tied to an economic benchmark like the Prime Rate, so if rates go up, your payments will too. This is the biggest risk with a HELOC—the dreaded "payment shock." A payment that feels perfectly manageable today could become a real financial burden if rates climb. It all comes down to what you value most.

Matching Your Goals to the Right Product

Deciding between a home equity loan and a HELOC is more than just a numbers game; it's about matching the right financial tool to your specific life goal. The best choice really depends on what you're trying to accomplish, your timeline, and how you feel about risk. To get it right, you have to look past the technical jargon and really picture how each one would work for you day-to-day.

Let's walk through some practical, real-world scenarios. We'll pinpoint situations where the stability of a home equity loan is a clear winner and others where the flexibility of a HELOC is exactly what you need.

When a Home Equity Loan Makes Perfect Sense

A home equity loan is your best bet when you have a large, one-time expense with a known cost. You know exactly how much you need, and you want a predictable payment that won't change. It’s all about simplicity and stability.

Think about these common situations:

- Major Home Renovations: You've got a firm $60,000 quote to finally gut and redo your kitchen. A home equity loan drops that full amount into your account, so you can pay your contractor and get started right away. Your monthly payment is locked in, which makes budgeting a breeze.

- Debt Consolidation: If you're tired of juggling multiple credit card payments with sky-high interest rates, a home equity loan can be a lifesaver. You can roll all that debt into one loan with a single, lower-interest payment. It simplifies your financial life and can literally save you thousands of dollars.

- Funding a Significant Expense: Need to pay for college tuition, a wedding, or a major medical procedure? These are perfect use cases. The lump-sum payout gives you the cash you need, all at once, and the fixed rate means you’re protected if interest rates go up later.

In the home equity loan vs HELOC debate, here's the bottom line: if your project has a clear price tag and a finish line, the predictability of a home equity loan is almost always the way to go.

When a HELOC is the Smarter Choice

A HELOC shines when your financial needs are spread out over time or are simply unpredictable. It’s less like a loan and more like a financial safety net—a revolving line of credit you can draw from whenever you need it.

Here’s where a HELOC really comes into its own:

- Ongoing Home Improvement Projects: Maybe you plan to build a deck this summer and then tackle the landscaping next spring. With a HELOC, you can draw funds for each project as it starts. You only pay interest on the money you’ve actually used, which is way more efficient than taking out a huge loan and letting cash just sit in your account.

- Establishing an Emergency Fund: Instead of parking a ton of cash in a low-yield savings account, a HELOC can act as a powerful emergency fund on standby. You have instant access to tens of thousands of dollars for a sudden job loss or medical crisis, and it costs you nothing until you draw on the line.

- Managing Fluctuating Business Expenses: For small business owners, a HELOC is an incredible tool. It can provide the working capital needed to manage uneven cash flow, buy inventory, or cover surprise costs without the hassle of applying for a separate business loan.

Both of these products let you tap into your home's equity at rates that are much better than unsecured debt. As of late 2025, the average American homeowner had about $213,000 in tappable equity. With home equity loan and HELOC rates often just above 8%, they are a far cry from the punishing rates of credit cards (over 21%) or even personal loans (over 11%).

Of course, lenders will look at your whole financial situation; if you want a better handle on this, check out our guide on how to calculate debt-to-income-ratio. The final cost of borrowing will always come down to your repayment plan and credit profile, as you can learn more about these rate comparisons on CBS News. By carefully matching the product to your goal, you can make sure you're not paying for flexibility you'll never use—or giving it up when you need it most.

How Market Conditions Influence Your Choice

The "home equity loan vs. HELOC" debate isn't just about your personal needs; the broader economic climate plays a huge role. Interest rates, specifically, can dramatically shift which product is the smarter, safer bet at any given time.

Think of it as another layer in your decision. You need to pick the right product for your goals, but you also need to pick the right one for the current financial environment. Timing your application with an eye on market trends can make a real difference to the long-term cost of borrowing.

The Impact of a Rising-Rate Environment

When interest rates are on the rise, predictability is king. This is exactly where a home equity loan has the upper hand. You lock in a fixed interest rate for the entire term, which means your monthly payment is set in stone from day one. It takes the guesswork out of budgeting and protects you from market swings.

A HELOC, on the other hand, becomes a riskier proposition in this kind of climate. Its variable rate is tied to a benchmark like the Prime Rate. As the Federal Reserve hikes rates to cool inflation, your HELOC payment will almost certainly climb right along with them, introducing an uncertainty many homeowners can't afford.

In a rising-rate climate, the stability of a fixed-rate home equity loan offers a powerful defense against unpredictable payment increases, making it the preferred option for risk-averse borrowers.

When Falling Rates Favor a HELOC

Now, let's flip the script. When economists expect interest rates to drop, a HELOC suddenly looks a lot more appealing. The very same variable rate that was a liability before becomes a major perk. As the Prime Rate falls, so does your HELOC's interest rate, leading to lower monthly payments over time.

You can learn more about how these market shifts create new opportunities by exploring our analysis of recent mortgage rate trends. In this environment, locking into a fixed-rate home equity loan could mean missing out on significant savings as borrowing gets cheaper. A HELOC lets you ride the wave down without having to refinance.

Recent trends show just how much homeowners are paying attention to this. With rates being so volatile, many have leaned toward the certainty of home equity loans. In fact, TransUnion's 2024 Mortgage Credit Industry Insights Report found that home equity loan originations shot up 13% year-over-year, reaching the highest volume in almost seven years. By comparison, HELOC originations only grew by 8%.

This data clearly shows a strong preference for the predictable, fixed payments of home equity loans in an uncertain market. You can dive deeper into the research on why home equity loans have become a better deal than HELOCs at Bankrate.com. It’s a perfect example of how much the economic forecast can sway borrowing decisions across the country.

Common Questions About Home Equity Financing

Even after breaking down the differences between a home equity loan and a HELOC, you probably still have a few questions. That’s completely normal. Making a decision that involves the roof over your head demands total clarity, and this is where we’ll tackle the most common concerns homeowners have.

Think of this as your final check-in. We'll cover everything from whether you can have both products at once to how the broader economy might affect your payments, ensuring you feel confident and ready for what's next.

Can I Have Both a Home Equity Loan and a HELOC?

Yes, you absolutely can. It's not uncommon for homeowners to have both a home equity loan and a HELOC simultaneously, provided you have enough equity to back both. Lenders look at your combined loan-to-value (CLTV) ratio to make their decision. This calculation lumps together your primary mortgage, the new home equity loan, and the full credit limit of the HELOC.

While this setup offers incredible flexibility—a lump sum for a big renovation and a credit line for unexpected costs—it also doubles down on the risk. You’d be juggling three separate housing payments, and a huge chunk of your home's value would be on the line. This path requires serious financial discipline and a rock-solid budget to avoid getting in over your head.

What Are the Typical Closing Costs for Each Option?

Closing costs are one of those practical details that can really swing your decision one way or the other. They are not the same for both products.

-

Home Equity Loans: Expect closing costs that feel a lot like your original mortgage, usually running between 2% to 5% of the loan amount. For a $50,000 loan, that’s $1,000 to $2,500 out of your pocket for things like appraisals, origination fees, and title searches.

-

HELOCs: This is where things get interesting. Many lenders advertise HELOCs with low or even zero closing costs to draw you in. But you have to read the fine print. They might charge an annual fee, or worse, an early closure penalty if you pay it off and close the account within the first few years (typically three).

Always demand a full, itemized list of fees for both options. A deal that looks cheaper upfront can easily end up costing you more down the road.

How Does My Credit Score Impact My Rate?

Your credit score is king here. It’s arguably the single biggest factor that determines not just if you get approved, but what interest rate you'll pay. A strong credit score tells lenders you're a reliable borrower, and they'll reward you with their best offers.

Most lenders want to see a score of 700 or higher to hand out their most competitive rates. You might still get approved with a lower score, but be prepared for a higher interest rate to offset the lender's perceived risk. Of course, they also look at your debt-to-income (DTI) ratio and how much equity you have. The perfect recipe for a great rate is a high credit score, low debt, and plenty of equity. It also matters who you borrow from; understanding the difference between a mortgage broker vs bank lender can reveal why different institutions might view your application differently.

What Happens if the Federal Reserve Raises Interest Rates?

This question gets to the heart of the risk difference between a home equity loan and a HELOC. How the economy behaves will affect each one very differently.

A HELOC is directly tied to market rates. Most have variable rates linked to a benchmark like the U.S. Prime Rate, which moves almost perfectly with the Fed. When the Fed hikes rates, the Prime Rate goes up, and your HELOC interest rate and monthly payment will climb right along with it. This is the gamble you take with a HELOC in an unpredictable economy.

On the other hand, a fixed-rate home equity loan is your shield against market volatility. Once you lock in your rate, it’s set in stone for the life of the loan. Your payment will be the exact same every single month, no matter what the Fed does. This predictability makes it a much safer bet when you're worried about rising rates.

Are you ready to build a rewarding career helping people navigate important financial decisions like these? At 24hourEDU, we make it easy to get your Mortgage Loan Originator license. Our online education is fully approved by the NMLS Nationwide Multi State Licensing System and Registry and includes our comprehensive exam prep package for free, giving you everything you need to succeed. Start your journey today at https://24houredu.com.

5 Comments